Our focus at Crawford Investment Counsel is on high-quality securities. This emphasis emanates from the philosophical underpinning of our approach to investing: the world is uncertain, and investing is risky. So, we seek to narrow the range of outcomes and improve our likelihood of success by owning shares of more predictable and consistent businesses, i.e., high-quality companies. We believe the higher level of visibility and safety that comes with a focus on higher-quality companies serves as a safeguard for our investors. And since we utilize the dividend as an initial marker of quality, we believe that our portfolios have an income stream that grows over time and actually increases purchasing power.

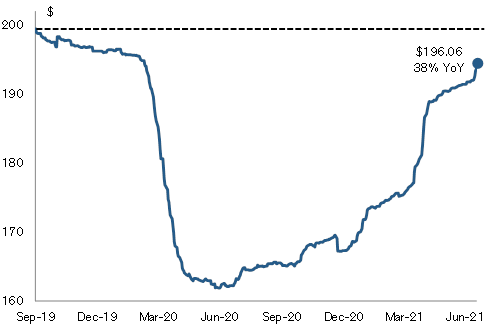

We recently came across a couple of interesting charts courtesy of Jon Golub, chief strategist for Credit-Suisse. The charts below illustrate the progression of earnings expectations for all of the S&P 500 constituents over the past seven calendar quarters. Going back to the fall of 2019, “consensus expectations,” as represented by Wall Street analysts, called for $200 per share of cumulative earnings in 2021. You may observe that as the pandemic led to an unprecedented economic shutdown which disproportionately impacted certain areas of the economy, profit expectations declined precipitously, dropping by some 25% to a low point of approximately $160. Now, just a year since earnings expectations for 2021 bottomed, those same estimates have almost fully recovered to pre-pandemic levels and are up approximately 25%.

Consensus Earnings Per Share Expectations for the S&P 500

Source: Earnings Revisions & Daily Update, Jonathan Golub, Credit Suisse Securities (USA) LLC (7/27/21)

The above chart illustrates that the future is indeed very difficult to predict, particularly on a shorter-term basis, and particularly for companies whose fortunes are highly sensitive to changes in overall economic activity. The quality factor we emphasize in our investment decision-making process tends to insulate us from some of the uncertainty and risk inherent to the market. Additionally, we believe it serves to shield us from big swings in earnings estimates, marking one of the reasons we find quality to be so valuable. It should not surprise anyone that the higher quality strata of the market saw earnings expectations decline much less during the economic shutdown, what we believe to be a direct result of the predictability, consistency, and lack of economic sensitivity of these higher-quality, dividend-paying companies.

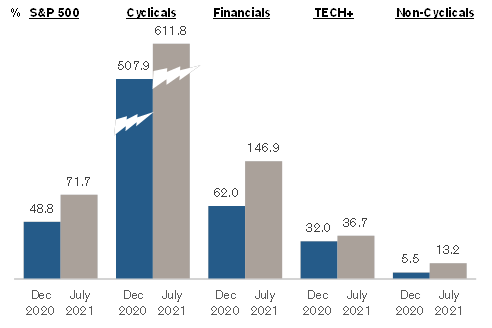

In fact, examining the changes in earnings expectations more closely reveals that the majority of the decline and subsequent recovery in profit expectations occurred within the cyclical portion of the market. The term cyclical implies a closer correlation with the business cycle and more reliance on the economy to produce end demand. These types of companies often cannot sustain their dividend payments in recessions, leading to disruption of income (see our piece INVESTING IN A RECESSION).

Conversely, we prefer to invest in companies that “control their own destiny” to a greater degree, and are more non-cyclical in nature, enabling not only uninterrupted dividend payments but in many cases, increasing payouts. You can observe below that these types of companies (non-cyclicals) have experienced very little change in earnings expectations.

Change in Earnings Estimates for 2021 by Sector of the S&P 500

Source: Earnings Revisions & Daily Update, Jonathan Golub, Credit Suisse Securities (USA) LLC (7/27/21)

In summary, earnings expectations for 2021 have made a round trip from $200 to $160 and now back to $196 per share. It’s no secret that more stable earnings and dividends are what we strive to seek over the longer term for our investors. We recognize the strength of this approach in periods of economic stress, and we are willing to accept the trade-off of less upward change in expectations in periods of recovery. We believe this is in the long-term interests of our investors.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-222

Watching & Waiting

As we move forward into 2023, Watching and Waiting seems an apt description of the posture of investors and where we find ourselves today.

The Incredible Shrinking P/E Ratio

The decline in share prices combined with stable earnings projections means Price to Earnings ratios have declined significantly over the past six months.

Prevailing Through Challenges: Interview with Small Cap Manager

We are really pleased with our strategy’s recent outperformance, because there have been several underlying trends in the market working against us.