Crawford Investment Counsel has a long history of investing in companies with what we believe to be consistent and predictable businesses, as evidenced by their dividend patterns. In fact, the firm’s inaugural large cap investment strategy, the Crawford Dividend Growth strategy, was founded on the concept of Dividend Integrity, which we define as a company’s ability to reward investors by sustaining and raising its dividend over time.

In the early 2000s, as we deepened our analytical strength and added capacity, we began to explore opportunities to expand the firm’s product suite while staying true to the core Dividend Integrity principle. Following the success of our initial efforts which focused on philosophical adjacencies in the large cap space, our team became intrigued by the possibility of applying the underlying principle to stocks at the lower end of the market capitalization spectrum.

Over time, Crawford’s research team observed that many companies at the low end of its investable market cap range often exhibited attractive fundamental characteristics and unusual consistency despite their small size. After performing extensive analyses and backtesting, we came to believe that the small cap area of the market represents a highly opportune space to apply our existing investment approach and achieve attractive, risk-adjusted returns.

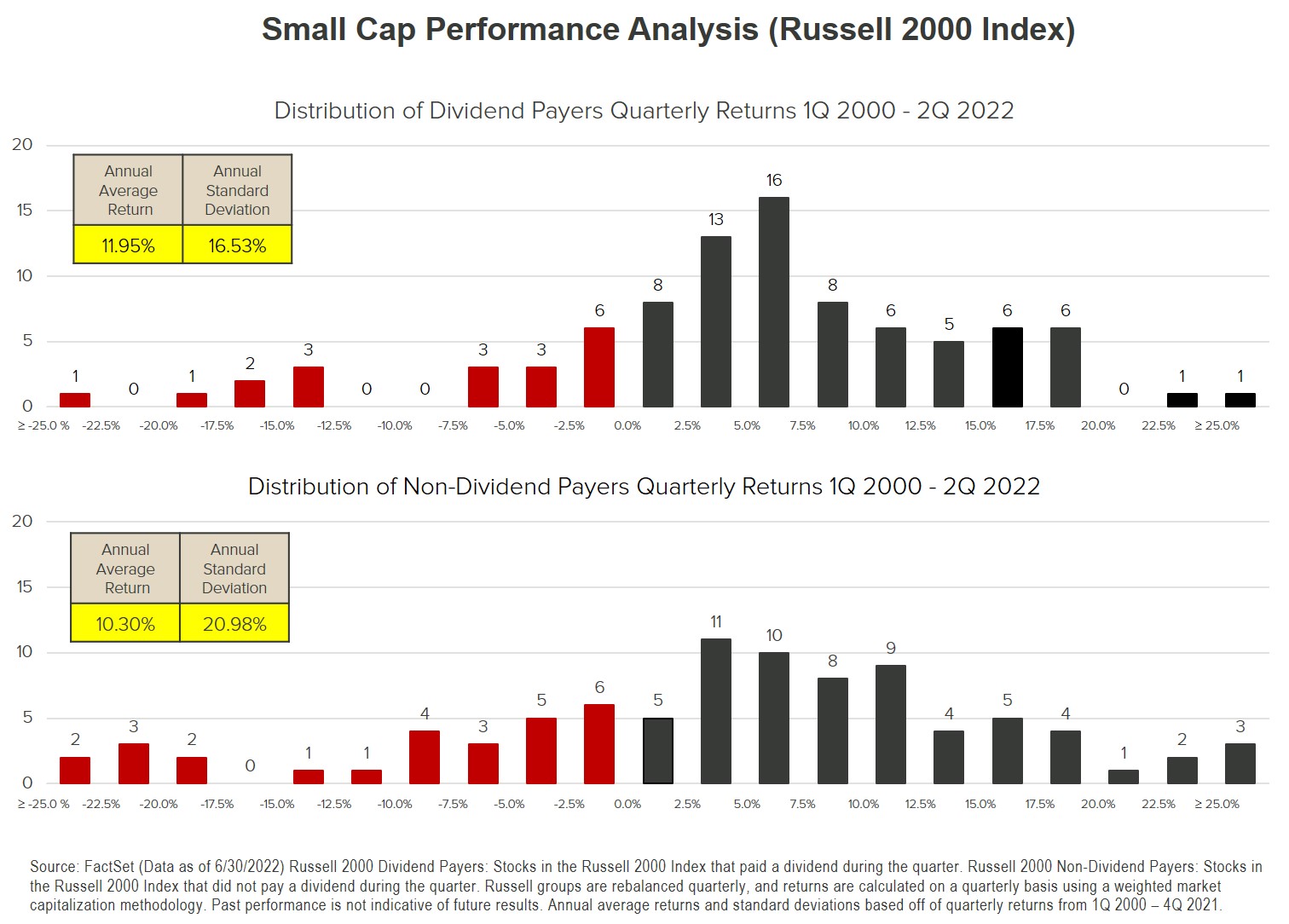

Crawford analyzed performance patterns of small cap stocks through the lens of the correlation between quarterly returns and a company’s dividend paying status. Crawford found that in the long run, not only did higher-quality small cap companies, as represented by their ability to pay a dividend, exhibit less volatility (especially on the downside), but also, and perhaps counterintuitively, these stocks provided superior overall returns. At Crawford, we believe this phenomenon is an extension of what we like to call the Dividend Effect.

The chart below provides the visual representation of this phenomenon. We can observe the much narrower dispersion of quarterly returns for dividend payers and a meaningfully lower number of quarters with exceptionally weak returns. The overall dividend payer return/risk advantage is summarized in the highlighted tables.

Essentially, Crawford recognized that the small cap area of the market enables diligent, high-quality, dividend-oriented investors to earn outsized returns. Moreover, we came to realize that this area of the market might actually be the best place to reap the benefits of our long-held philosophy, and we launched the Small Cap strategy in 2012 to capitalize on this golden opportunity.

Crawford has always held the belief that the ability of a company to regularly pay and sustain dividends is highly consistent with other desirable investment characteristics such as balance sheet strength, consistent and ample free cash flow generation, low earnings variability, and high return on equity. Secondary attributes often include strong management teams, low capital requirements, and sound capital allocation practices. We believe that these quality characteristics are particularly important when investing in small cap companies, as they provide important downside protection benefits in a highly volatile market segment.

Another reason why the Dividend Effect is particularly prominent in the small cap area of the market is the apparent behavioral investor bias against more stable, dividend-paying small cap companies. Our experience suggests that most small cap investors seek high reward opportunities by betting on “the next big thing” while underestimating the inherent risks of these speculative investments. This bias is further inflamed by Wall Street incentive structures geared towards capital-raising activities for immature companies and provide little accountability for investor losses. As a result of this investor neglect, high-quality small cap companies often trade at attractive valuations – a market inefficiency Crawford seeks to exploit.

While the Dividend Effect is one of the more persistent and durable factors leading to successful small cap investing, it cannot replace the need for exhaustive research of individual companies included in investors’ portfolios. This is where Crawford’s time-tested stock selection process truly shines. With dividend-paying history as an excellent starting point, our dedicated team of seasoned professionals seeks to identify companies with the most attractive fundamentals that are underappreciated by the market. This process involves extensive analysis of historical financial statements, assessment of a company’s strategy and competitive position, conversations with management teams, evaluation of industry trends, and valuation scrutiny. The outcome of this process is a diversified, high-conviction portfolio set up to deliver attractive returns with below-average volatility. With the 10-year anniversary of the Small Cap strategy quickly approaching, we are proud to report that we have delivered on these objectives. In fact, the table above demonstrates that Crawford’s Small Cap strategy has outperformed its opportunity set while taking on less risk.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

The composite returns are shown as supplemental information to the Small Cap Equity composite disclosures regularly distributed by the firm. If you have not received a copy of Crawford’s GIPS composite reports, please contact Casey Krimmel Dhande at Crawford Investment Counsel, 600 Galleria Parkway, Suite 1650, Atlanta, GA 30339.

The widely recognized benchmark(s) are used for comparative purposes only. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000 Index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The volatility (beta) of the portfolios may be greater or less than the benchmarks. It is not possible to invest directly in these indices.

CRA-22-213

The Perpetual Accumulation Approach: Can You Have Your Cake and Eat It Too?

At Crawford, we believe that by investing in quality, employing a price sensitive approach, and establishing reasonable spending policy, our investors can have their cake and eat it too.

Don't Be Fooled By Dividend Hubris

Not all dividend-payers possess Dividend Integrity, and some actually exhibit what we call Dividend Hubris.

Prevailing Through Challenges: Interview with Small Cap Manager

We are really pleased with our strategy’s recent outperformance, because there have been several underlying trends in the market working against us.