With real Gross Domestic Product (GDP) registering declines in the first two quarters of the year, the popular definition of a recession was achieved. Due to special circumstances such as big moves in inventories and trade – two factors that do not indicate underlying weakness in the economy – most observers are discounting this as a special situation. The strong belief is that the National Bureau of Economic Research (NBER), the official body that designates the beginning and end of recessions, will not consider this to be the beginning of an official recession. We agree with this assessment but, at the same time, are not willing to completely ignore the fact that these two quarterly declines in economic activity have meaning. Thus, while we believe that the economy is not in a recession, it behooves us to be alert to the possibility of one developing in the near-to-intermediate future, and to consider possible causes.

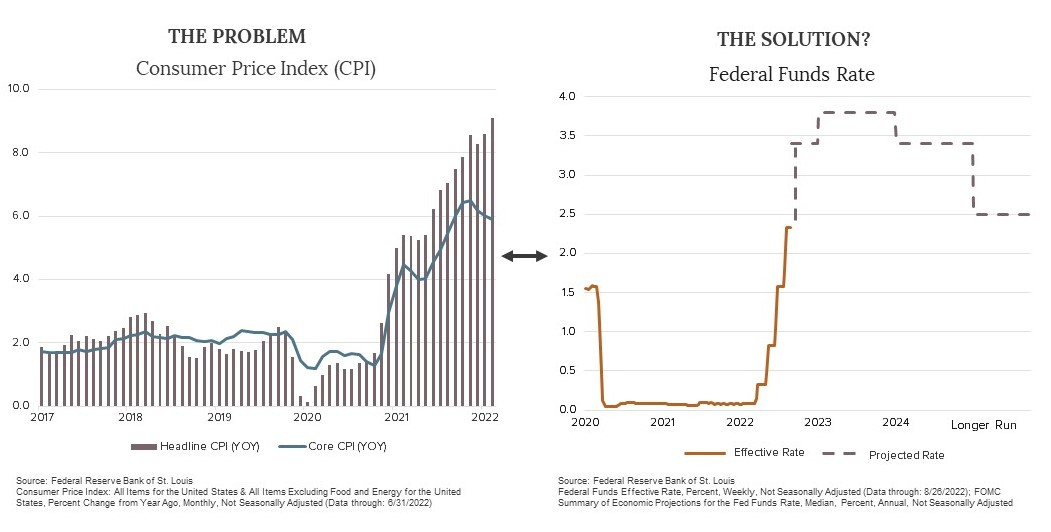

We believe the biggest threats to the economy are the presence of very high rates of inflation and the fact that the Federal Reserve (Fed) has committed to bring inflation back to its target of 2%. This is a big task, one that is fully understood by the Fed. Chairman Jerome Powell said of the Fed that “our responsibility to restore price stability is unconditional.” The use of the word unconditional means they have no choice but to succeed, no matter the cost. The nature of the fight is displayed below in these two charts.

The latest inflation reading, 8.5% year-over-year for July, is an extraordinary number for a mature economy. Even though it declined from 9.0% the previous month, and on a month-over-month basis was an encouraging 0%, it is still a long way from 2%. There is a lot of work left to do. The Fed produces forward guidance on their expected interest rate increases, and as revealed above, they expect the federal funds rate to reach 3.8% by the end of 2023. Actually, since the last release of their planned federal funds increase they have shifted emphasis away from formal guidance, instead saying that they will be “data dependent.” This means they will review data on inflation and react accordingly. It also implies that they are not sure exactly what will be required to achieve the desired results.

Within the context of the possibility of the economy falling into a recession, there are a number of risks, not the least of which is a policy error by the Fed. As they pursue the fight against inflation by raising interest rates and shrinking their balance sheet, they are attempting to dampen demand enough to eventually bring inflation down to their 2% target. The risk in calibrating policy is the lag time for policy changes to actually begin to affect the economy. It is assumed that this time lag is twelve to eighteen months. But if the Fed is being “data dependent,” that means they are looking at current conditions and extrapolating their policy for the next year and a half. There is plenty of room for disconnect.

A quick review of history does not suggest the likelihood of the Fed doing “just enough” and thereby achieving a “soft landing.” That term is a salutary one, for it suggests that the Fed can reduce demand just enough to gradually bring inflation down while keeping the economy moving ahead. If achieved, it will be a deft move. It is not impossible, for it has been done in the past, but more often than not, the error has been for the Fed to go too far by underestimating the effect of policy moves, thus dampening aggregate demand too much and pushing the economy into recession.

A part of the riskiness of a policy error lies in the assumptions about the neutral rate of interest. The Fed considers this theoretical rate to be around 2.5%. The belief is that when most economic factors are in balance, a short-term interest rate of around 2.5% will keep them there. At that level, policy rates are considered to be neutral – neither expansionary nor contractionary – and will enable the economy to keep growing with stable inflation and full employment. However, with all things theoretical, we can only assume they are correct. If they are wrong and in fact the neutral rate is higher, then policy that is assumed to be neutral will in fact be stimulative. Conversely, if the assumed neutral rate is lower and rates are higher, then policy will be contractionary. All this illustrates just how difficult it is to successfully conduct monetary policy and how it is subject to error. As noted above, pulling off a “soft landing” is not impossible, but to do it successful probably requires at least some measure of good luck. In the current circumstances we are wishing the Fed lots of luck.

Again, we do not believe we are in a recession. Furthermore, there are reasons to assume that a recession can be avoided, for there are considerable strengths in the economy at this time. Consumer balance sheets are in very good shape, suggesting that aggregate demand can be sustained. Wages are increasing, and if inflation continues to recede, these wage gains will turn real. Also, the labor market remains very strong with unemployment of 3.5% at a fifty year low. These economic factors support our assumption that we are not in a recession, and if we are to have one, it will not develop in the near future. But over the intermediate term, we have to acknowledge that there is a risk of recession, most explicitly because of the possibility of a policy error by the Fed. It behooves us to keep monitoring conditions for signs of emerging recession, and that we will be doing. We will keep our readers updated as to what we see.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

CRA-22-219

Interview with the Dividend Growth Portfolio Manager

Our strategy is a great fit for investors who are seeking a value-oriented approach that does well when markets are strong and protects when they are weak.

Not Diversification, Dividendification!

We seek diversification by investing across various areas and sectors of the market, and we insist on dividendification in the name of achieving successful outcomes for our clients.

The Uncertainty of Investment Returns

As a stock market investor, there are few guarantees. However, we believe if one has a well thought out discipline and remains invested, suitable results follow.