In a world where information flow is both immediate and constant, we recognize the need to step back in the interest of maintaining proper perspective. Similar to investing, having a framework for analyzing and interpreting economic data can improve the likelihood of successfully figuring out what is taking place and where the economy is headed. Financial news networks tend to encourage shorter-term decision making. We want to take this chance to emphasize what we believe to be the importance of keeping our focus on the long term. This leads us to focus on a small number of key readings of economic activity, which we refer to as “The Big Four.”

The Big Four are outlined below along with some thoughts on current readings and an overview of where we believe the economy is headed today.

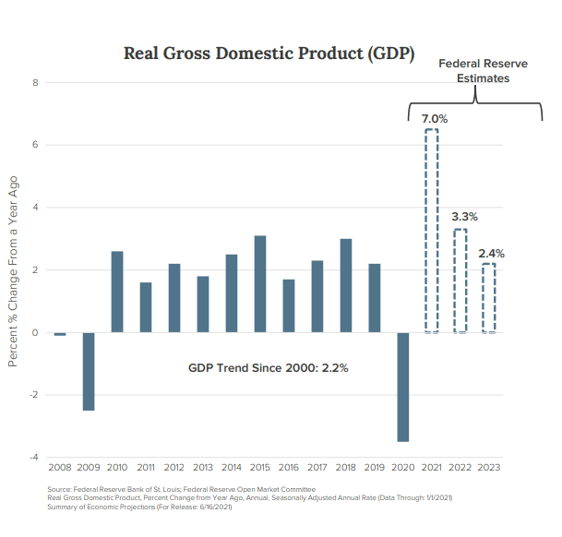

- Gross Domestic Product – The basic measure of the economy’s output of goods and services

- The collapse we witnessed in March of 2020 has been followed by an almost “boom-like” rebound.

- Reopening of the economy is providing a robust, post-COVID environment powered by excess savings and continued fiscal and monetary support.

- The rate of recovery may be peaking right now –we believe growth will continue but at a slower pace. Projections are for the economy to settle back to near its sustainable growth rate of something like 2% by 2023.

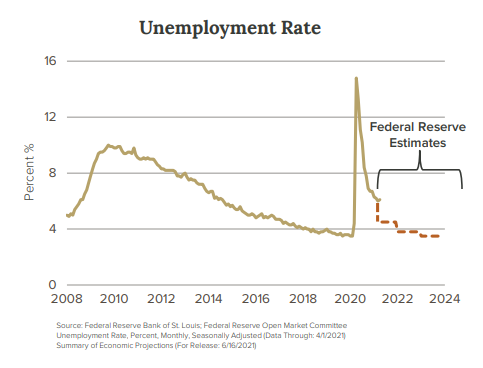

2. Employment – Growing employment means more money in workers’ pockets, which fuels consumption

- After peaking at near 15%, unemployment has declined sharply to its current rate of 5.8%. Full employment is considered to be around 4%.

- As GDP growth continues, it is logical to expect full employment to be reached in 2022. Once unemployment benefits expire in September, the pace of employment gains should quicken.

- A low rate of unemployment is essential to the health of the economy. We believe things are currently moving in the right direction.

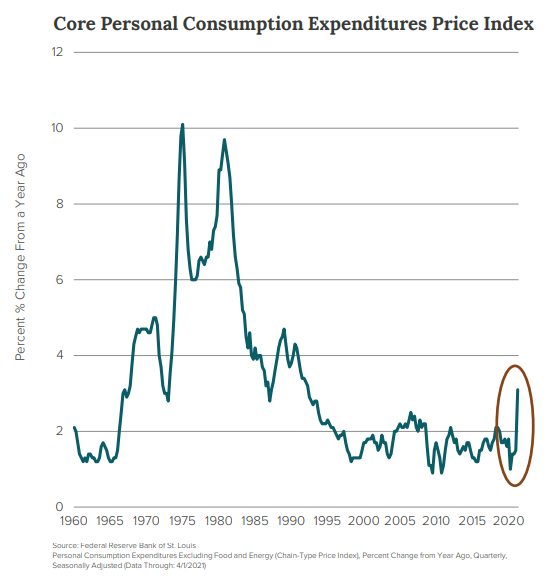

3. Inflation – Low and stable inflation improves confidence and preserves purchasing power of consumers

- Inflation has been in a downtrend for some 40 years to the benefit of the economy and financial markets.

- Currently, inflation measures are rising due to base effects of the 2020 collapse and dislocations caused by the reopening of the economy. The Federal Reserve (Fed) believes these increases will be transitory. We tend to agree.

- Inflation is influenced heavily by the supply/demand equation. For years there has been a worldwide excess of supply, which has tended to keep inflation under control. There is no conclusive evidence that this relationship has changed.

- We retain our belief that there are a number of secular forces keeping inflation under control.

4. Interest Rates – Low and stable interest rates encourage borrowing, which in turn stimulates economic activity

- Inflation and inflation expectations ultimately decide where interest rates settle. This is why we believe the era of low interest rates is not over.

- If the sustainable growth rate of the economy is around 2%, long-term rates have room to rise somewhat but not dramatically.

- As long as the Fed maintains short-term rates at zero, longer-term rates are limited in terms of their ability to rise.

While we do maintain our focus on the Big Four, we give an honorable mention to the Purchasing Managers Index (PMI). This is an index of the prevailing direction of economic trends in the service and manufacturing sectors. At its essence, the index summarizes whether market conditions as viewed by purchasing managers are expanding, contracting, or staying the same. For some of the reasons outlined above, we feel that this indicator is especially pertinent today in predicting current and future business conditions.

The Big Four provides a framework for our thinking, enabling us to continue to take a long-term approach to investment decision making.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Forward looking statements cannot be guaranteed. This document may contain certain information that constitutes “forward-looking statements” which can be identified by the use of forward-looking terminology such as “may,” “expect,” “will,” “hope,” “forecast,” “intend,” “target,” “believe,” and/or comparable terminology. No assurance, representation, or warranty is made by any person that any of Crawford’s assumptions, expectations, objectives, and/or goals will be achieved. Nothing contained in this document may be relied upon as a guarantee, promise, assurance, or representation as to the future.

CRA-21-209

Bursting the Bubble: Speculative Fervor Then & Now

Long-term success comes from staying disciplined, avoiding speculative frenzies, and focusing on remaining invested in high-quality investments that can weather the test of time.

Porter’s Five Forces in the Crawford Equity Research Process

We apply Porter’s Five Forces of critical thinking to each potential investment for CIC equity strategies.

GDP: The Economy Surprises Again

For now, we celebrate the outstanding performance of GDP. The future is not risk free, but for now, the present is pretty good.