Passive investing has seen a decade-long increase in popularity. It is appealing because of the lower fees and convenience provided by large mutual fund companies. While passive investing appears to be serving investors adequately, we see underpinnings of deterioration.

A large problem with passive investing is crowding. It is quite easy to invest passively, as millions of investors are able to purchase a couple thousand dollars of an index fund on a weekly basis over several years. What continues to be less clear, and is a large risk factor, is what happens when investors want their money back during a downturn.

In addition, we are skeptical that passive investors know what they own. One of the most popular passive strategies is to buy an index that mirrors the S&P 500. Investors wanting more growth augment with a sub-index of technology or other growth stocks. This behavior has led to crowding within the S&P 500, which may be beginning to unwind.

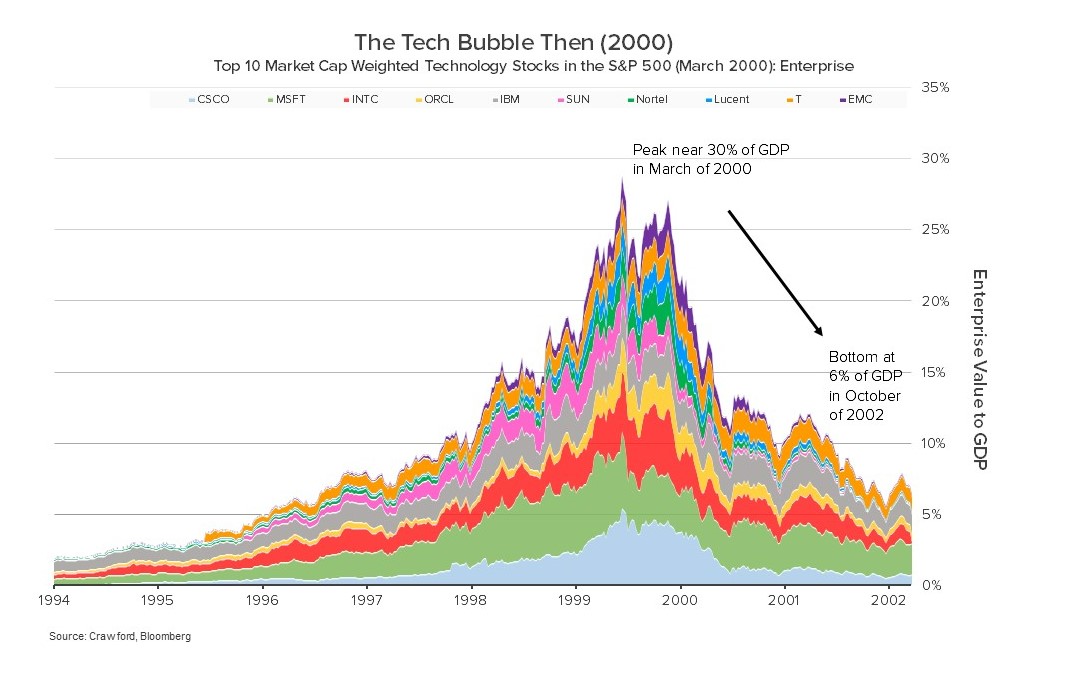

Crowding occurs when investors prefer specific investments and bid up the price of those investments to unsustainable levels. In the U.S., the last time crowding was a major factor was in the Tech bubble of 2000. The chart below shows the value of the largest positions in the S&P 500 compared to the gross domestic product of the U.S. This peaked at approximately 30% on March 27, 2000, which is an incredible amount of wealth concentrated in very few companies given an economy as diversified as the United States.

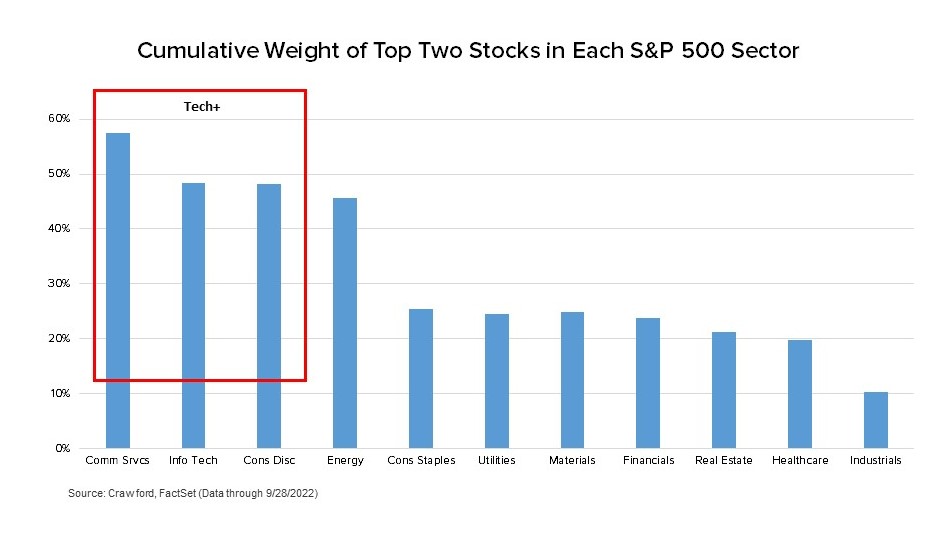

There is currently a similar situation. The chart below shows the concentration of the two largest stocks in each sector for the S&P 500. The data shows concentration not only of the S&P 500 index, but also the greater potential pitfall of the passive investing strategy of 80% S&P 500 and 20% S&P 500 Information Technology (ticker: XLK). That strategy would currently have 10.4% invested in Apple and 9.1% invested in Microsoft, given the large market capitalization of those two companies. This leads us to a concerning question, can a portfolio be diversified if it has two positions that occupy nearly 20% of the portfolio’s capital?

For the last thirteen years, owning large positions in large capitalization growth stocks has been a winning formula. But the same could have been said about owning growth technology stocks for the seven years prior to 2000. We do not know the future, but such large positions make us uneasy.

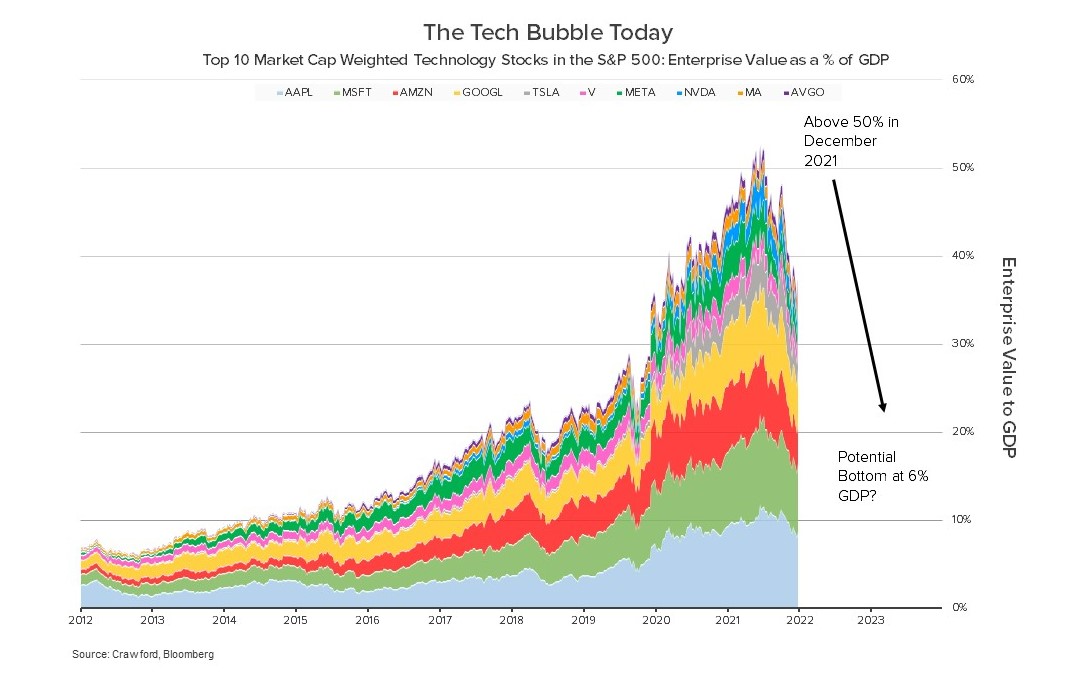

To put the current environment in perspective, the S&P 500 is more crowded today than in 2000. In 2021, the enterprise value of the top ten companies as a percentage of GDP topped out at 52%. Even after a 24% sell off from the high in December 2021, the top ten technology companies are still greater than 30% of GDP. Moreover, the top five companies – Apple, Microsoft Alphabet, Amazon, and Tesla – currently have an enterprise value greater than 25% of GDP. The concentration is still greater today than in 2000, a warning sign for investors.

At Crawford Investment Counsel, diversification and transparency are essential. For our clients, we actively monitor portfolios for position size and other risk factors to ensure that no company, industry, or economic driver could de-rail our clients’ investing goals. From a transparency perspective, we buy individual stocks, purposefully put together in portfolios tailored for our clients’ needs. This allows each client to easily know exactly what they own and the income from each position.

While passive investing may have served some investors over the last decade, we view now as the time to reconsider active investing. At Crawford Investment Counsel, we have helped our clients survive the ups and downs of the market for over forty years with quality, dividend-paying stocks as the backbone to their portfolios.

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. The S&P 500 Index is the Standard & Poor's Composite Index and is widely regarded as a single gauge of large-cap U.S. equities. It is market-cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-246

The Total Shareholder Return Trifecta

We invest to achieve an investment trifecta by selecting stocks that provide our investors with all three components of total investment return: fundamental business progress or growth, dividend yield, and valuation improvement

Example of Investment Thesis: AstraZeneca

In the first installment of the Company Fundamental Investment Series, Senior Research Analyst and Director of Core Equity Strategy, Frank Pinkerton, walks us through an investments thesis.

Uncertainty is Certain

Life is filled with uncertainties, and this reality actually serves as one of the basic premises for Crawford Investment Counsel’s investment philosophy.