In this piece, we take key points from our firm's most recent Bond Policy Meeting and share them with our readers. Hopefully, this piece will provide some insight into the economy and fixed income markets and give you a sense of how our team is thinking about recent trends and developments.

Crawford Bond Policy

- Nominal Treasury yields moved higher across the curve between the July and September Fed meetings. The increase in 5-year and longer maturity yields can be attributed to:

- Higher Real yields, reflecting an expectation for the Fed to maintain its target rate for an extended period of time, and

- The resurrection of term-premium (additional yield compensation for longer-term securities) last seen prior to the financial crisis.

- Investment-Grade Corporate bond spreads have been unchanged since our July bond policy meeting despite significant new issuance volume in September. This is supported by an overall drop in year-to-date issuance of ~ 3%.

- Spreads are currently below the 1-year and 30-year+ averages. This has been a meaningful contributor to our relative performance.

- Spreads are currently below the 1-year and 30-year+ averages. This has been a meaningful contributor to our relative performance.

- The high-grade Municipal bond market has outperformed taxable securities since our July bond policy meeting.

- It remains at historically low relative value levels versus comparable Treasury securities across the yield curve.

- Absolute yields are attractive, however, reaching levels last seen in 3Q22 and 10 years prior.

- Chairman Powell's press conference following the Fed meeting was “hawkishly” optimistic with an improved economic outlook and lower inflation and unemployment projections:

- The labor market remains tight but supply and demand conditions continue to come into “better balance.”

- The economy has been expanding faster than expected this year. Consumer spending has been “particularly robust,” and housing has “picked up somewhat.”

- Inflation “remains well above the longer-run goal of 2%.” There’s a “long way to go” in the process of getting inflation down.

- Rate Policy: “It’s certainly plausible that the neutral rate is slightly higher than the longer-run rate."

- Powell stated: “A soft landing is our primary objective… That’s what we have been trying to achieve.”

- Chairman Powell communicated that the Fed is now in a very good place to react to incoming data through policy decisions. The Fed's decision to leave the fed funds rate unchanged is likely more of a “pause” than a “skip”. Timing policy precisely in this final stretch of working inflation down will be challenging. The difference between achieving a soft landing and tipping the economy into recession is marginal.

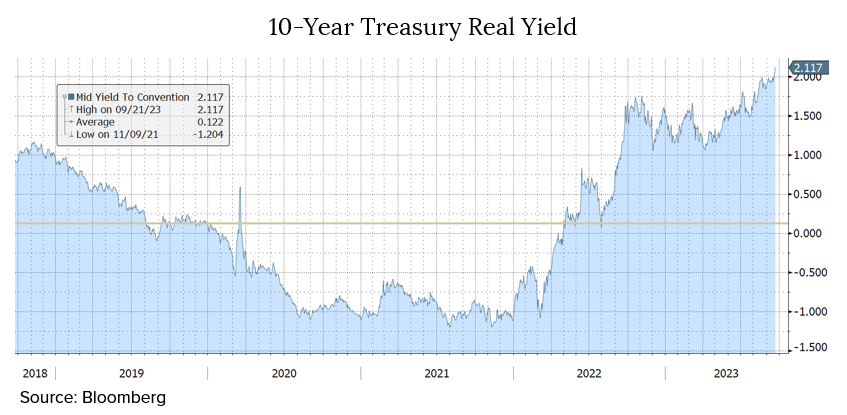

- Bond market performance since the June Fed meeting suggests the economy has transitioned from a supply-constrained, stimulus-driven inflationary environment to a more traditional cyclical growth environment where the real economy is accelerating. This is illustrated by the rise in real yields.

- Our policy is to maintain the average effective maturity of our strategies at the longer end of our intermediate investment horizon. We will maintain our bias to “defensive” corporate market issuers, tax-backed and essential service municipal issuers, and government agencies. We are hopeful for an economic soft landing but mindful of the potential for recession.

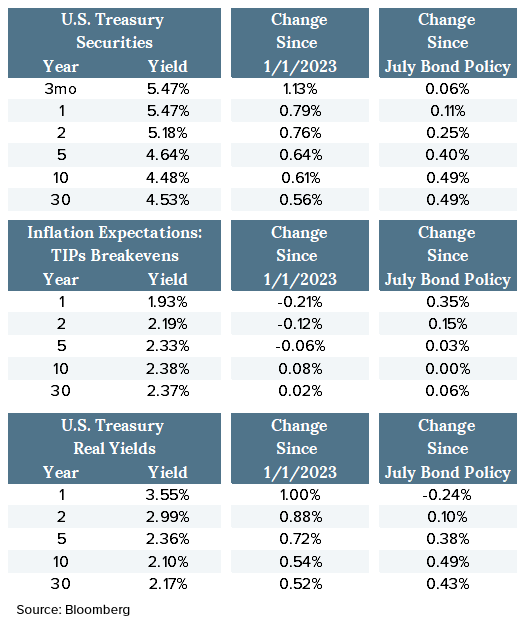

Treasury Yields as of 9/21/2023 (Post-Fed Meeting)

- Nominal Treasury yields moved progressively higher across the curve since our July bond policy meeting.

- The 3-month/10-year Treasury yield curve inversion (beginning in November 2022) flattened by ~43 basis points, and the 2-year/10-year Treasury yield curve inversion (beginning in July 2022) flattened by ~23 basis points.

- Market inflation expectations, as reflected in TIPs (Treasury Inflation Protected securities) “Breakevens,” were mixed with expectations moving higher in the 1- to 2-year range, while intermediate and longer-term expectations were essentially unchanged.

- Real yields fell in 1-year Treasuries but rose meaningfully in the 5- to 30-year range.

- Treasury yields moved higher between the July and September Fed meetings as economic growth prospects outweighed concerns surrounding potential impact from additional tightening. This yield move was specifically driven by an increase in Real Yields, reflecting market expectations for:

- The Fed to maintain the terminal federal funds rate for a longer period,

- Consideration for the potential impacts of secular changes in the economy, and

- The term premium required to compensate investors for uncertainty surrounding U.S. Government deficit growth and increased financing costs.

- Current and near-term issues that could cause economic disruption and uncertainty include:

- The UAW strikes

- Potential Government shutdown

- The resumption of student loan payments, and

- High energy prices

- BRICS - geopolitics

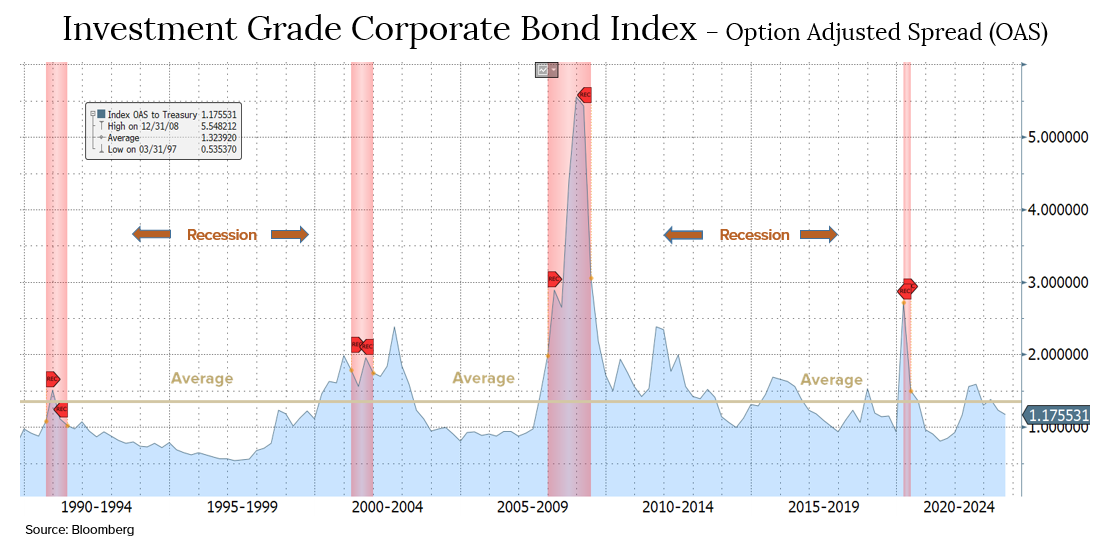

Corporate Bond Market - Option-Adjusted Spread (OAS)

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- Investment Grade Corporate OAS is essentially unchanged from our July bond policy meeting (recent peak was March 15th at +163).

- Spreads remain tight, currently trading ~15bps below the 30-year average of +132 and ~17bps below the 1-year average of +134.

- The graph below illustrates that spreads typically widen leading up to a recession and peak during a recession.

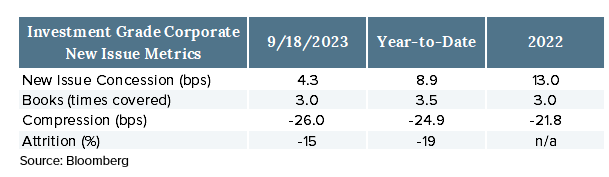

Corporate Bond Market - Bond Issuance & Financials

Technical Support

- Spreads have been supported by strong demand, as illustrated in new issue statistics and retail fund flows.

- Lower new issue supply (down ~3% year-over-year) has also supported tight spreads.

- Attractive absolute yields continue to be the most important metric supporting the demand-side of the high grade corporate market.

- Overall, investment grade corporate fundamentals are strong:

- EBITDA margins have improved,

- Leverage metrics were flat across the first and second quarters,

- Cash balances were up over 9% year-over-year in the second quarter, supported by a 29% drop in share repurchases and a slowdown in non-Financial dividend growth.

- Interest coverage ratios have weakened:

- Non-Financial ratios fell in the second quarter, primarily due to rising interest expense. This will continue to be a challenge for companies with substantial maturity walls over the next few years if interest rates continue to hold in a “higher-for-longer” environment.

- Non-Financial ratios fell in the second quarter, primarily due to rising interest expense. This will continue to be a challenge for companies with substantial maturity walls over the next few years if interest rates continue to hold in a “higher-for-longer” environment.

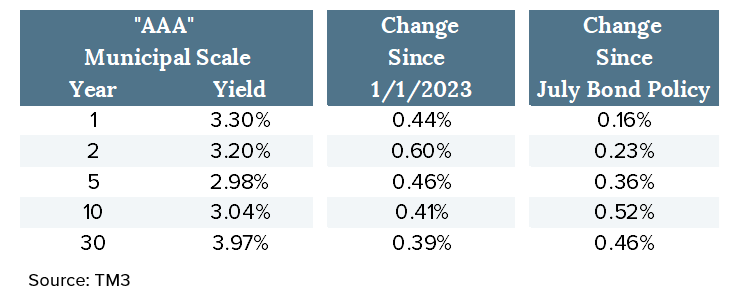

Municipal Bond Market

- Municipal bond yields moved significantly higher between the July and September Fed meetings, primarily in sympathy with Treasury yields.

- The typical summer redemption cycle of insufficient new bond issuance to meet maturity redemption reinvestment demands continued to support municipal bond prices, and relative value metrics remained at historically tight levels.

- Absolute yields in the municipal market are attractive, however, and continue to provide a compelling alternative to Corporate bonds on an after-tax basis.

The Market's "Higher for Longer" Narrative

Conclusion: Real Yields reflect an economic transition from a supply-constrained, stimulus-driven inflationary environment, to a more traditional cyclical growth environment where the real economy is accelerating. Absent the global savings glut experienced in the post-financial crisis cycle, interest rates have moved higher. This reflects secular change, real growth potential, a higher Fed Funds neutral rate, and investors’ demanding term-premium.

- Real Yields reflect investor return expectations based on economic growth absent the eroding effects of inflation. Forces influencing real yields include:

- The Fed Funds Rate: a base for real yields, the Fed Funds rate is expected to be higher in the future to accommodate:

- The general strength of the U.S. economy despite high interest rates, exhibited by the growth in business investment (manufacturing construction) with the largest GDP contribution in four decades.

- Secular shifts in the economy which reduce savings, including:

- Deglobalization: the reversal of secular disinflation from Chinese manufacturing leading to onshoring higher labor expenses;

- Demographics: aging workers retiring from the large Baby Boomer generation resulting in a smaller labor force and nest egg spending (also increase deficits with increased Social Security and Medicare spending).

- Government fiscal management which demands higher investor compensation:

- Higher debt levels: forecasted to reach 118% of GDP by 2025 (3x higher than the median “AAA” sovereign),

- Larger projected deficits: the federal deficit is up 170% in the first nine months of the fiscal year vs. the same period in the prior year,

- Higher interest costs: the cost of servicing Government debt rose 25% in the first nine months of the fiscal year,

- Shrinking investor base: banks have a diminished appetite, the Fed is shrinking its holdings, and foreign buys have faded (e.g., China/Japan).

- The general strength of the U.S. economy despite high interest rates, exhibited by the growth in business investment (manufacturing construction) with the largest GDP contribution in four decades.

- The Term Premium: investor compensation for risk associated with a long-term security, is believed to have recently become positive after being stuck at 0% over the decade following the financial crisis. Rate volatility and the shift to a higher level of interest rate and inflation uncertainty are forcing an increase in yield compensation.

- The Fed Funds Rate: a base for real yields, the Fed Funds rate is expected to be higher in the future to accommodate:

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-169

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

December Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.