The overall direction of the domestic economy is determined by many factors, not the least of which are monetary and fiscal policy. In recent years monetary policy has been the dominant influence on the economy, but for several reasons the emphasis is shifting to the fiscal side. Because of the needs of the economy emanating from the pandemic and historically low interest rates, new ways of thinking about fiscal policy are being considered in the policy arena. Some policymakers are advocating for very aggressive fiscal policy on the grounds that the cost of financing government debt is more important that the amount of debt that is issued. This shifting emphasis toward fiscal policy could materially impact economic activity in a positive way in the years to come.

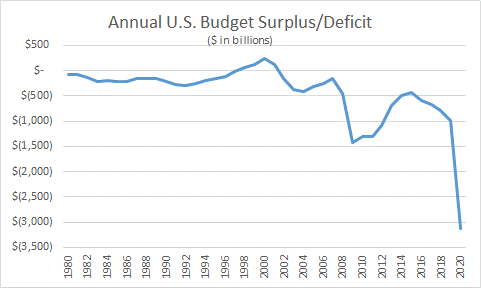

What exactly is fiscal policy? Simply, fiscal policy is a change in government spending. Governments will attempt to stimulate economic growth through government spending that creates budget deficits or limit government spending in order to bring budget deficits into better balance. Budget deficits at the federal level are regular occurrences. The chart below indicates that the U.S. government has not had a balanced budget in 20 years, and in fact, the deficits have been getting progressively worse.

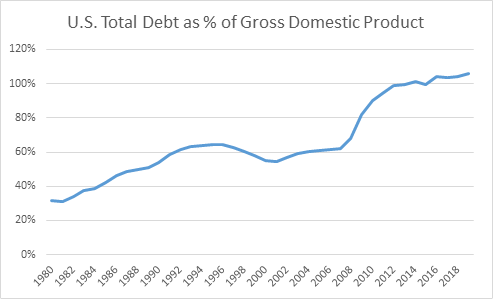

When the U.S. Government runs a deficit, it is financed by issuing government debt. With swelling deficits, a tremendous amount of U.S. Government debt has been issued, leading to the question, how much debt is too much? This is one of the eternal questions on which there is no consensus. Probably the best way of thinking about how much government debt is outstanding is to compare it to Gross Domestic Product (GDP), which measures the size of the economy. Over the last decade or so there have been three major events that have caused a surge in government debt as a percentage of GDP: (1) the financial crisis and ensuing Great Recession (2009-2012); (2) the Trump tax cuts (2018-2019); and (3) the COVID economic collapse (2020+). As indicated in the following chart, the result of these three episodes is an increase of government debt as a percentage of GDP from around 60% to over 100%. This has been alarming to many, raising fears that either inflation will surge or that an excessive amount of government debt will crowd out private borrowing. To date, neither condition has developed, although there is no guarantee they never will.

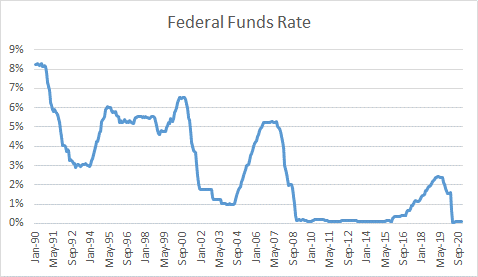

Monetary policy is under the direct control of the Federal Reserve (Fed). The Fed, independent of the executive or congressional branches, essentially works to achieve “maximum employment, stable prices, and moderate long-term interest rates.” Its chief policy tool is the federal funds rate which can be raised to combat inflation or lowered to stimulate growth and employment. Currently, the federal funds rate resides near zero, or what is referred to as the zero bound. Unless the Fed were to adopt negative interest rates, something they say they will not do, federal funds cannot go any lower. The Fed has other tools to impact economic activity, namely, quantitative easing, forward guidance, and yield curve control, but the federal funds rate is by far the most important one. At near zero, the Fed’s ability to further stimulate the economy is limited. It is mainly for this reason that the focus is now switching to fiscal policy as the primary tool for both relief and stimulus.

A number of economists argue that with low interest rates and a forecast for sustainably low rates, fiscal policy should not be restricted by fear of rising amounts of debt. Accordingly, the government should be borrowing to keep the economy going in the absence of the private economy being able to do so, as the interest payments are relatively low versus the impact of the stimulus on the economy. Consider that if the current Biden relief bill of $1.9 trillion were to be enacted in addition to previous relief bills, total COVID-related expenditures would be around $5 trillion. However, financed at 1% or less, there is only an increase in annual debt maintenance costs of $50 billion. If these expenditures are temporary, as opposed to tax reductions that are permanent and add to the deficit every year, they can be tolerated. Some economists go further to encourage aggressive fiscal policy on an ongoing basis with the idea that sufficient growth would be created to justify the added debt. On an ongoing basis, if the rate of growth in debt is lower than trend rate of growth of the economy, debt as a percentage of GDP will be contained.

These views are becoming more widespread among economists, not the least of which is Janet Yellen, the new Secretary of the Treasury. In her confirmation hearing she said, “But right now, with interest rates at historic lows, the smartest thing we can do is act big.” Secretary Yellen is clearly behind the idea of aggressive fiscal policy. She is now a part of the Biden administration and as Secretary of the Treasury will be advocating for the administration’s economic policies. Her new role at Treasury puts her in a different position than when she was Fed Chair, where she was operating as the head of an independent agency.

Janet Yellen brings considerable bona fides to her position as Secretary of Treasury in addition to being the first woman to hold the Treasury Secretary position. She has experience at the White House as Chair of the Council of Economic Advisors under Bill Clinton, as well as being a past Chairperson of the Fed. Well educated as a graduate of Brown and Yale Universities, she is of the Keynesian school of economics, believing that markets and economies are not perfect and thus need to be limited or stimulated by government intervention. Her inclination toward aggressive fiscal policy at this time is in accordance with her Keynesian beliefs.

An additional advantage is that Secretary Yellen and current Fed Chair Jerome Powell have worked together in the past and have a good working relationship. When she was Fed Chair he was a Fed governor, so they have direct experience working together. Chairman Powell has also been public with his view that the pandemic-burdened economy needs more aid.

The debate over proper fiscal policy is currently focused on relief. The pandemic has the U.S. economy under pressure, and many individuals and small businesses need aid. Further relief is expected as the economy works its way toward more normal circumstances. Once the economy is back to normal, the discussion will shift from pandemic relief to longer-term stimulus, including the President’s commitments on the campaign trail to infrastructure investment. The term investment implies an economic return on expenditures. Infrastructure investments seem to be one of the more obvious choices for longer-term stimulus, despite being expensive and adding to future deficits. A key determinant for long-term economic growth will be the return on the debt through more capital spending, new jobs, and increases in productivity, thereby justifying the fiscal expenditures. The debate will go on, but for now, and until interest rates normalize, fiscal policy is where the action is.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request. This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed.

CRA-21-044

Alpha When You Need It Most

At Crawford, our strategies have far lower risk than the major market indices as measured by beta. And not only do our strategies have far lower risk, but they also produce positive alpha.

Why Dividends Matter: Downside Protection

One of the more favorable aspects of investing in dividend-paying stocks is their ability to help protect capital in declining stock markets.

Is Your Portfolio Ready for Winter?

Currently, there is a dramatic shift occurring in the global financial markets. Unlike a fantasy novel, it is not as definitive as the first snowfall.