Utilities meet several objectives within Crawford Investment Counsel portfolios, including attractive current income with low earnings variability as well as a growing environmental, social, and governance (ESG) focus. The consistency found within utilities is a function of the fact that it is a regulated industry that enjoys fairly constant and growing demand. This steady growth helps foster modest yet predictable dividend growth.

But first, a quick refresher on utilities. At Crawford Investment Counsel, we primarily focus on regulated utilities. This type of utility is regulated by the respective state commission where they do business. Most aspects of the company are set via local commissions that determine the range of returns each utility is allowed to earn including its capital structure and any revenue increases. This helps ensure that not only the company and shareholders earn an attractive return but also ensures an essential service is delivered to customers at a fair price. Most regulated utilities are vertically integrated, meaning they generate their own power, transmit the power through company-owned lines, and distribute the power to consumers and businesses.

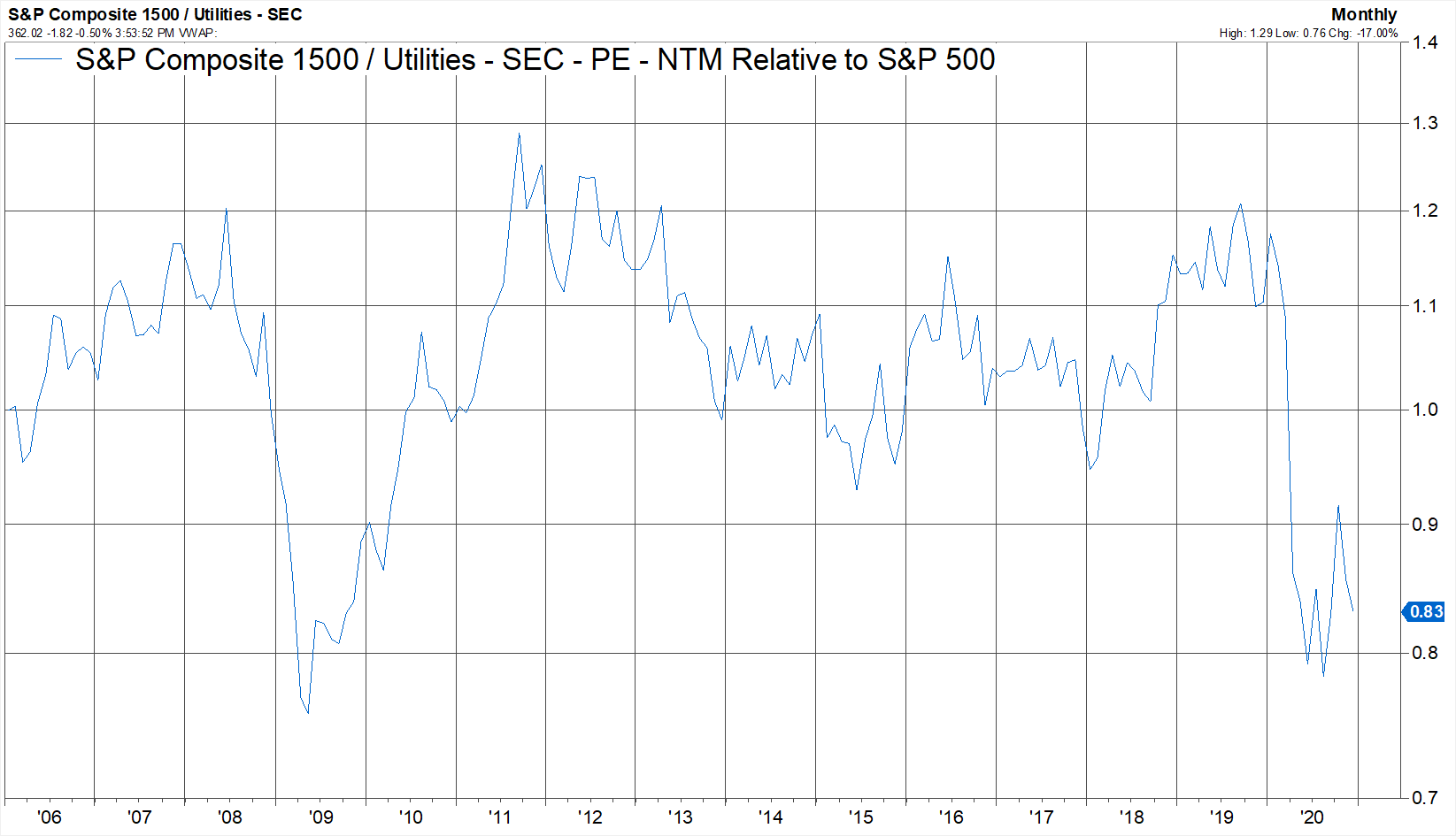

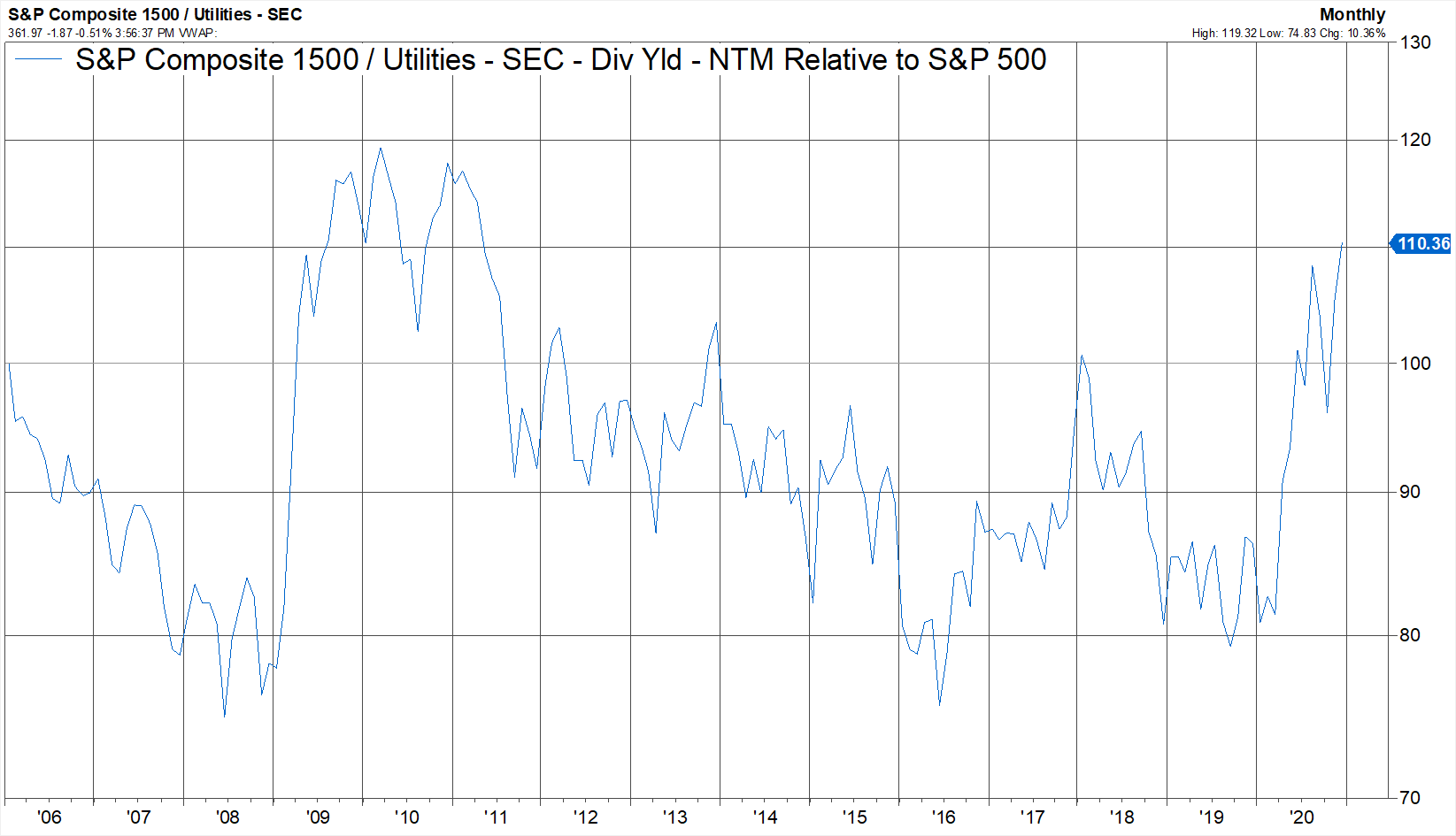

Heading into 2021, the utilities sector is particularly attractive from a valuation and income perspective. As shown below, utilities are attractively valued versus the S&P 500 and U.S. Government Bonds. In fact, utilities have not been this cheap relative to the S&P 500 outside of the Great Financial Crisis in 2009. Consequently, utility dividend yields are materially higher than the S&P 500’s dividend yield and U.S. Government Bond yields.

Source: FactSet

Source: FactSet

Bad Debts and Inflation Fears

Due to the pandemic, some state regulators banned customer cutoffs for non-payment, which negatively impacted the sector. However, most utilities have recovery mechanisms in place or are working with regulators on recovery of these bad debts via future rate case filings with regulators. We believe this issue will be resolved in 2021.

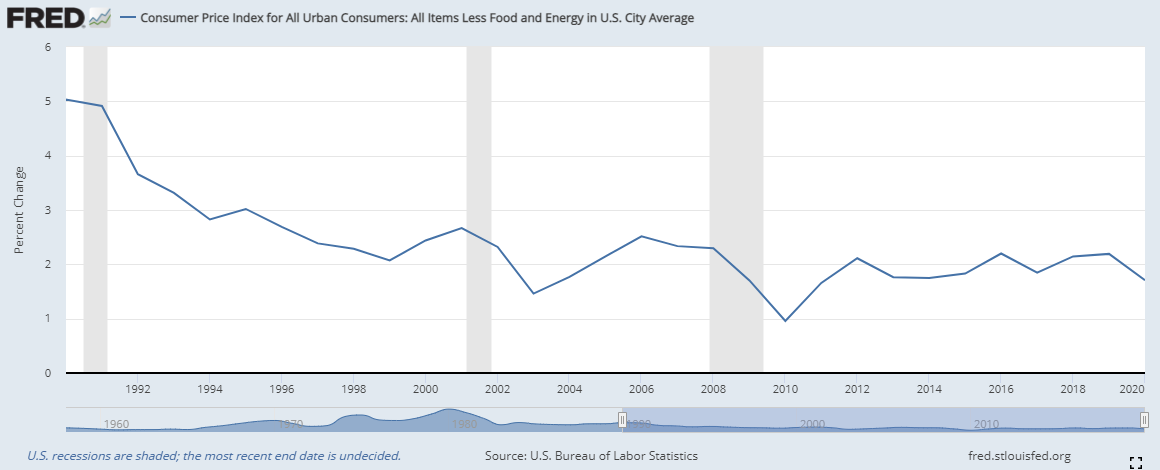

Fears of inflation have also impacted sentiment for utilities from time to time, but we continue to believe the data does not support it. As shown below, the U.S. Consumer Price Index (CPI) has been in a downtrend since 1990. As a result, the Federal Reserve has indicated it will keep the Federal Funds rate at zero until they reach their objective of 2% average CPI. This is relatively bullish for higher-yielding securities such as utilities.

Coal Burn Out

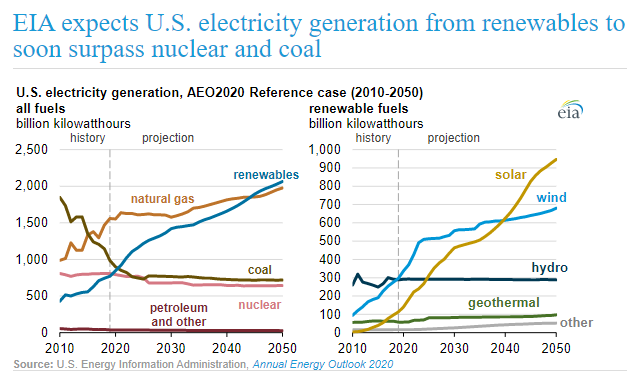

In 2000, coal was 50% of the U.S. fuel source for power generation, which has been cut in half today. In 2019, natural gas accounted for 38% of the nation’s electricity, followed by coal at 23%, nuclear at 20%, wind at 7%, hydroelectric at 7%, and other renewables at 4%. According to the US Energy Information Ad-ministration (EIA), power generation from renewables will surpass coal for the first time in 2021. While a huge accomplishment in and of itself, utilities earnings will also increase from these investments. Utilities are achieving cost savings from retiring inefficient coal plants and replacing them with a free generation source, namely the sun and wind. As a result, consumers are not getting a large increase in power bills due to these conversions. This is a true win-win-win scenario.

In summary, utilities meet all of the objectives we seek to realize at Crawford Investment Counsel. Utilities provide a growing current income stream at a reasonable price as well as a focus on sustaining and improving our environment.

Disclosures

Published July 2020. The opinions expressed are those of Crawford Investment Counsel. The opinions referenced are as of the date of publication and are subject to change due to changes in the marker or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford investment portfolio. Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. This data is for informational purposes only and is not intended to serve as investment advice or tax advice, to be relied upon as a forecast or research. These findings of these studies and the potential value-added benefits may not equal or exceed the actual experience of the client. The information provided is for illustrative purposes. The investment or strategy discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Past performance does not guarantee future results. It is recommended that clients consult with their tax professional for specific tax-related questions.

Forward-looking statements, including without limitation any statement or prediction about a future event contained in this presentation, are based on a variety of estimates and assumptions by Crawford Investment Counsel, including, but not limited to, estimates of future operating results, the value of assets and market conditions. These estimates and assumptions are inherently uncertain and are subject to numerous business, industry, market, regulatory, geo-political, competitive and financial risks that are outside of Crawford Investment Counsel’s control. There can be no assurance that the assumptions made in connection with any forward-looking statement will prove accurate, and actual results may differ materially. The inclusion of any forward-looking statement herein should not be regarded as an indication that Crawford Investment Counsel considers forward-looking statements to be a reliable prediction of future events.

Crawford Investment Counsel, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Crawford’s advisory services can be found in its Form ADV which is available upon request. CRA-20-111

Why Dividends Matter: Income & Growth of Income

When all the attractive attributes of dividends are considered, among the most favorable is the fact that the income component of total investment return is always positive.

Watching & Waiting: The Return to the 2% World?

If the 2% world is considered to be the normal world, why are we so far off the mark, and what are the underlying conditions that would make it normal again?

The Great Debate: Income Vs. Total Return

One of the contested issues in financial planning is whether income generated by investments matters beyond its contribution to total return...