The Crawford Investment Counsel (CIC) Small Cap strategy aims to deliver attractive investment returns over the long run while reducing the volatility associated with investing at the lower end of the market capitalization range. We strive to accomplish this objective by constructing a portfolio of what we believe to be high-quality, smaller-sized companies with solid growth prospects that are underappreciated by other market participants.

The process of selecting stocks for this portfolio entails a rigorous research effort by our team of experienced analysts who possess deep sector knowledge, a philosophical commitment to quality, and emphasize traditional fundamental analyses.

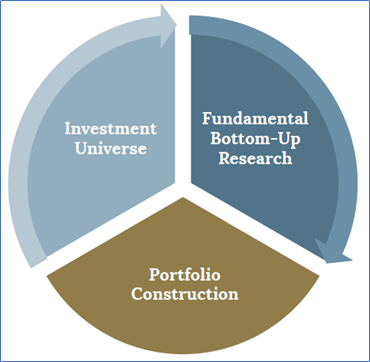

At a high level, the process consists of three key steps:

1. The initial screening of the investable universe;

2. Analysis of individual companies by sector analysts;

3. Evaluation of investment ideas by the entire investment team;

Below we review each of these steps in more detail:

SCREENING

At this stage, the goal is to narrow our potential investment choices to a subset of companies with what we believe to be above-average quality characteristics. We begin by identifying all U.S.-traded stocks with a market value between $100 million and $5 billion and, consistent with our long-held view that dividends are an excellent indicator of quality, we zero in on companies that have at least a 3-year dividend-paying history. This yields a list of approximately 800 stocks, which we refine further by utilizing several quality factors that apply to companies regardless of their economic sector. These factors include earnings variability (a measure of business cyclicality and profit resiliency through an economic cycle), return on equity (a measure of business profitability), and cash flow return on invested capital (a measure of capital intensity and the company’s ability to convert accounting profit into cash). The end result is a high-quality focus list of 120 – 150 stocks that is used for more in-depth evaluation by sector analysts and is the primary source of new investment ideas.

FUNDAMENTAL ANALYSIS

This step in the stock selection process involves comprehensive analyses of business trends, financial characteristics, and growth prospects of investment candidates within each analyst’s coverage. This is the most time-intensive and labor-intensive part of the entire process, but we believe it is indispensable to successful investing.

Our analysts take full advantage of all available information sources such as regulatory filings, financial statements, management presentations, industry-level and economy-level statistical data, as well as research published by Wall Street firms. While we look at a large number of quantitative metrics to assess a company’s financial health, we also evaluate qualitative aspects of the business such as product differentiation, management quality, and overall competitive standing. The ultimate goal here is to identify companies that we believe can generate superior long-term earnings and cash flow growth with below-average volatility.

Simulations Plus (SLP), one of the portfolio’s successful multi-year holdings, is a good example of the type of businesses we seek. SLP is a provider of highly specialized software and services to the pharmaceutical industry that allows for more efficient research and development of new medicines. The company enjoys a dominant market share in several therapeutic niches and benefits from growing research outlays by the biopharma industry, which are generally not dependent on the economic cycle. Furthermore, approximately 65% of SLP’s revenues is derived from subscription-type fees, which supports earnings stability. Thanks to a highly scalable business model, the company generates top-tier profitability and strong cash flow. SLP’s quality characteristics are rounded out by its unique intellectual property, zero-debt balance sheet, and a well tenured management team that includes the company founder.

In addition to rigorous fundamental analyses, our research process takes into consideration a stock’s valuation as we look for businesses that we believe are mispriced relative to their peers and/or relative to their quality and growth characteristics. Crawford analysts typically compare current valuation multiples such as price-to-earnings, enterprise value to EBITDA, or price-to-book to historical trading patterns. When appropriate, discounted cash flow models are also utilized to ascertain the intrinsic value of the company under consideration. While we realize that high-quality businesses rarely trade at cheap valuations, market participants with short investment horizons or a less than full understanding of the company in question frequently overreact to temporary business setbacks resulting in attractive purchase opportunities. Furthermore, given the scarcity of widely-distributed research on small cap stocks, many investors may not be fully aware of the creation of value opportunities at specific companies.

Once an analyst has identified a promising investment candidate that has an attractive combination of business fundamentals and valuation, an investment thesis would be developed. This is the rationale for stock outperformance and inclusion in the portfolio. A thesis would typically be based on the expectation of an inflection point in the company financial performance or valuation associated with any number of factors like entry into new markets, development of new products, internal operational improvement, business combinations, management changes, or changes in industry structure, to name a few. In conjunction with thesis development, the analyst would make a projection of the stock’s total shareholder return (TSR) potential over the following 3-5 years. TSR calculation is based on the projected earnings growth, dividend payments, and expected valuation improvement and is helpful in comparing investment ideas across economic sectors.

The fundamental analysis step of the stock selection process culminates in the writing of a formal, detailed report, which is then distributed to all investment team members for evaluation and consideration. At this point, the process becomes more collaborative as it moves into the portfolio construction phase.

PORTFOLIO CONSTRUCTION

The involvement of the entire eight-member team in vetting new ideas allows us to benefit from the combined expertise and perspectives of our team members as we scrutinize investment candidates from many different angles. It is not uncommon for smaller-sized companies to operate in several adjacent markets that do not necessarily conform to typical industry classification or sector norms. For example, many technology companies serve industrial, consumer, or health care customers, and financial companies provide services to customers across every economic sector. With team members coming from a variety of professional backgrounds, each one brings a unique perspective that further strengthens our analytical capabilities.

Typically, a team discussion of a purchase candidate results in a list of questions and concerns that the sponsoring analyst would subsequently address in a follow-up note. Once the idea is fully vetted, the purchase decision is made by the Director of Equity Research, the Strategy Director, and the sponsoring analyst. While we employ a flexible approach to position sizes, which range from 50bps to 250bps (0.5%-2.5%), the initial position size is driven by the relative strength of the investment case.

The end result is a focused, yet diversified portfolio of 60-70 high-conviction investments that we believe are well positioned to meet the strategy objective of generating attractive, risk-adjusted returns.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

Past performance is not indicative of future results. All investments carry a certain degree of risk of loss, and there is no assurance that an investment will provide positive performance over any period of time. This material is distributed for informational purposes only. This is not a recommendation to buy or sell a particular security. There is no assurance that any securities, sectors or industries discussed herein will be included in or excluded from an account's portfolio at the time you receive this report or that securities sold have not been repurchased. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or individual portfolio needs.

CRA-21-042

Insights from the Equity Research Team

In this piece, we take recent commentary from various members of the Equity Research Team and share it with our readers.

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

Quality Comes Into Favor as the Fed Pivots

With some emerging concerns about a softening economy, quality is being emphasized to a greater extent, and since this is the predominant characteristic of our portfolios, this has been reflected in the returns.