Crawford Bond Policy

- Nominal Treasury yields moved higher across the curve since our June 15th, 2023 bond policy meeting due to real yields outpacing a drop in market inflation expectations.

- Continued strength in economic data coupled with the market digesting an increased likelihood in the “higher for longer” Fed funds narrative drove real yields up and pushed inflation expectations down.

- Investment-Grade Corporate bond spreads tightened since our last bond policy meeting based on improved demand metrics in the new issue market and improved issuer credit fundamentals.

- The Municipal bond market remains very expensive observing generic yields on a relative value basis.

- We remain patient and focused on both absolute yield levels and relative value as measured in terms of yield spread (vs. the “AAA” GO scale) and percentage of comparable maturity Treasury securities.

- We continue to have success (particularly in the new issue market) in maintaining a discipline to selectively extend our effective maturity distribution @ 3% or better yields.

- The current “calendar effect” with maturity redemptions significantly outpacing issuance is expected to abate beginning in September.

- Chairman Powell's press conference following the Fed meeting reiterated more than it revealed:

- The labor market remains “very tight,” with the demand for labor continuing to exceed supply

- The economy is expanding at a “moderate” pace – which is an upgrade from “modest”

- Inflation has “moderated somewhat,” but has a “long way to go”; longer-term inflation expectations remain “well anchored”

- Policy has not been “restrictive enough for long enough” to do the job in durably reducing core inflation

- Powell reiterated policy will be conducted on a “meeting by meeting" basis with decisions driven by the “totality of the data”

- One significant change Powell revealed in the press conference was the fact that Fed staff economists are no longer forecasting a recession. This is significant because of what it implies about the strength of the economy, and because Powell openly disagreed with their assessment in his May press conference.

- We continue to believe there is a higher likelihood the economy will fall into recession rather than experience a soft landing.

- We believe the likelihood of a soft landing has meaningfully increased and acknowledge the strength of consumer and corporate balance sheets as a powerful force in extending the traditional lag associated with monetary tightening impacting demand.

- Ultimately, demand will have to be brought in balance with supply in the economy. This is what the Fed is pursuing in its fight against inflation.

- With respect to investor demand for high-yielding short-term securities, we acknowledge the value those securities currently offer. However, given our conviction regarding the likelihood of a recession, and our total return objective, we will continue to maintain a bias for locking-in attractive yields at the longer end of our intermediate maturity spectrum.

- Recession timing is not predictable with a high degree of certainty. Whether we experience one 6 months or 2 years from now, the result will be lower yields and our strategies will benefit from a total return standpoint.

- Reinvestment risk in short-term securities remains too high in our opinion.

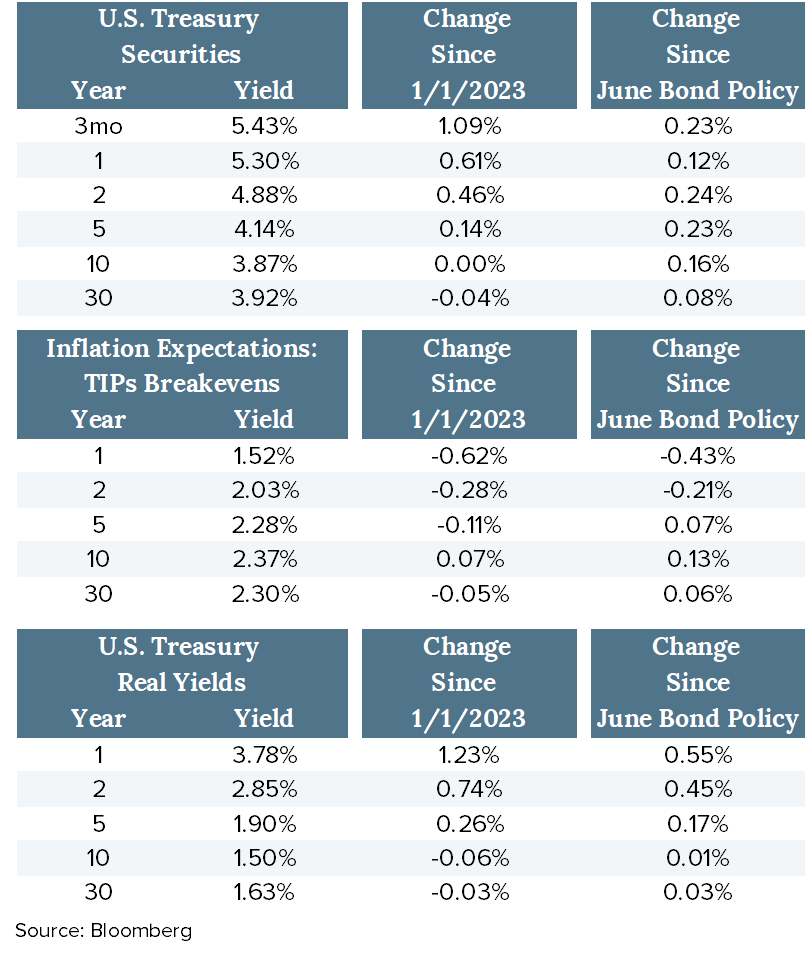

Treasury Yields as of 7/26/2023 (Pre-Fed Meeting)

- The narrative driving Treasury yields higher across the curve since June 15th is focused on the increase in short-term Real Yields. This reflects the market's expectation for the Fed to maintain a higher terminal federal funds rate for longer than previously expected.

- This also explains the decrease in short-term inflation expectations, because a federal funds rate that is "higher for longer" is likely to slow economic activity enough to reduce inflation.

- Support for the Fed's ability to keep its policy rate higher for longer is based on the strength of consumer and corporate balance sheets. Refinancing over the course of the post-Financial Crisis and pre-COVID cycle, when Fed policy was anchored for years in the 0%-0.25% range, has positioned consumers and corporations to weather the substantial increase in interest rates we have experienced since March 2022.

- Fiscal stimulus during the COVID pandemic also significantly contributed to the bolstering of personal and corporate finances.

- If there is a potential for a “soft landing” this cycle, it will likely be attributed to the strength of consumer and corporate finances and the Fed not having to go to an extreme policy level fighting inflation.

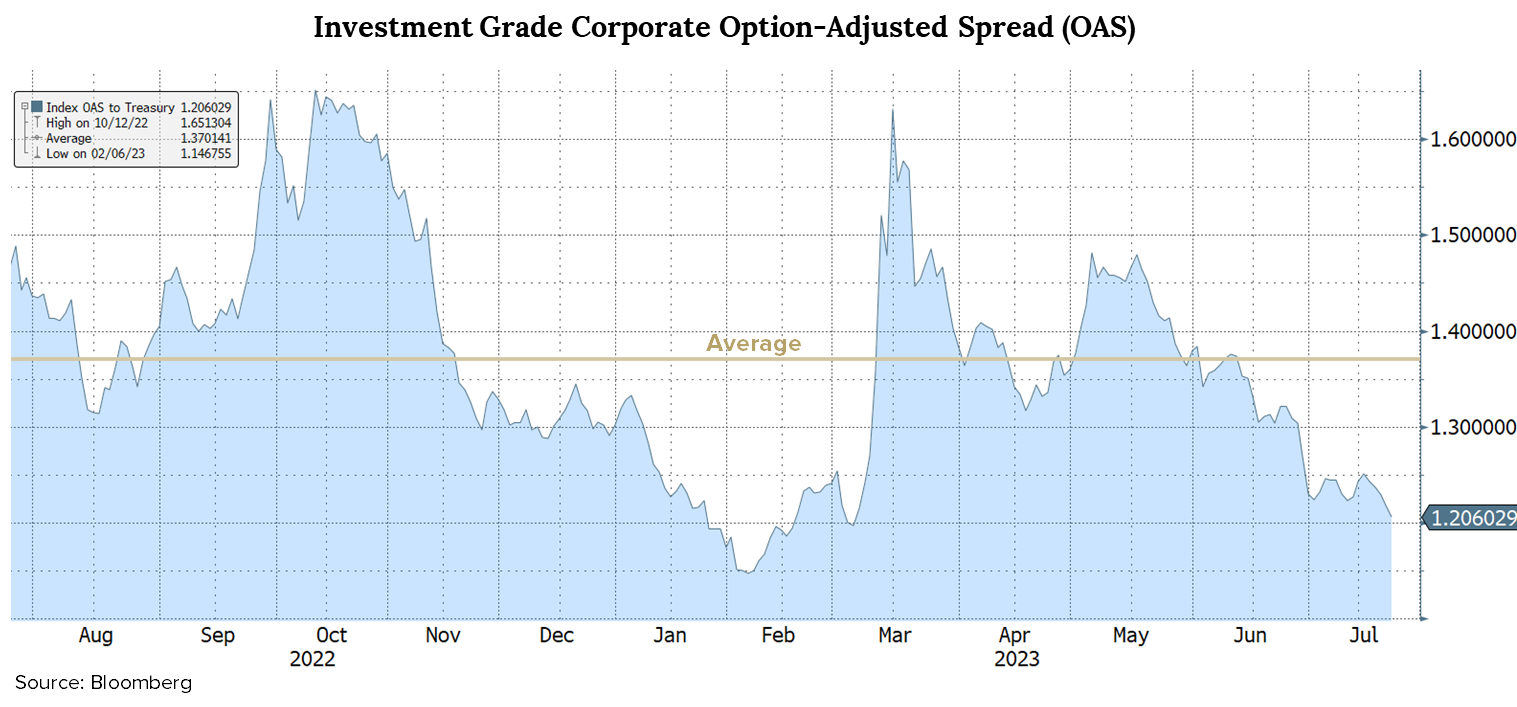

Corporate Bond Market - Option-Adjusted Spread (OAS)

- Investment-Grade Corporate Option-Adjusted Spread (OAS) evaluates the additional compensation investors require for credit risk being taken above a risk-free treasury security.

- Investment-Grade Corporate OAS has tightened roughly 10 basis points to +122 since our June 15th meeting (recent peak was March 15th at +163).

- This recent move was driven by positive sentiment from macro data and a solid start to the second quarter earnings season.

- Spread volatility is low, which has translated into tighter spread levels with a decline in perceived risk.

- Historically, rising real interest rates coupled with below-average to declining GDP growth has forced spread levels wider.

- The apparent difference in this cycle is demand supported by attractive absolute yield levels and corporate balance sheets made strong by post-financial crisis refinancing and economic strength.

- We believe spreads will widen if the economy turns down, however, the magnitude will likely not be to the same degree experienced in previous recessions.

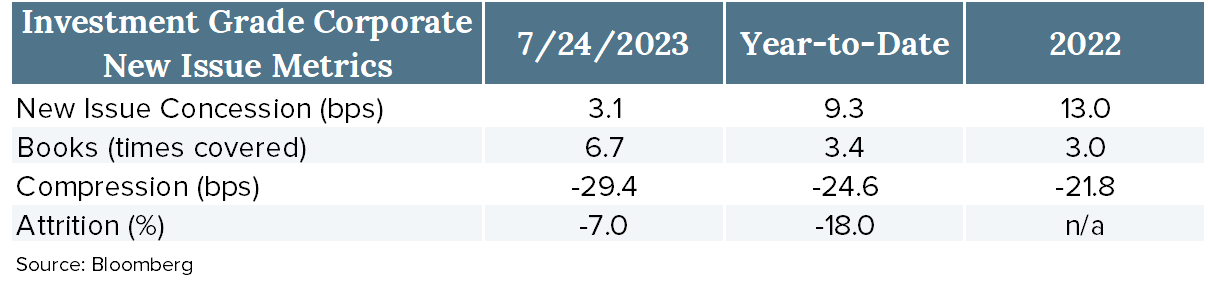

Corporate Bond Market - Bond Issuance & Financials

Technical Support

- New issue demand metrics continue to improve and show impressive strength given the backdrop of uncertainty regarding the stage of the economic cycle

- Issuers are paying significantly less yield to attract buyers, as illustrated by the drop in new issue concession, and order books have recently jumped in subscription level

- After more than a year of deterioration, investment-grade credit metrics have improved, including Leverage (Net Debt / EBITDA), which peaked in late 2020

- This improvement helps justify the conundrum of yield spreads, which have not appeared to fully reflect the volatility in the bond market and lack of clarity regarding the economic outlook

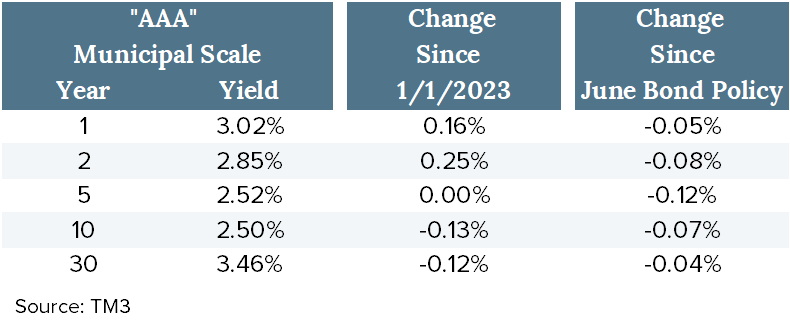

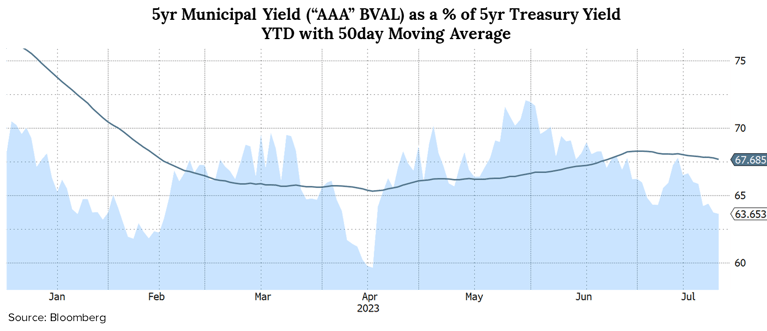

Municipal Bond Market

- The municipal bond market has continued to outperform U.S. Treasury securities with the support of seasonal reinvestment needs and consistent credit quality

- The redemption graph illustrates the anticipated decrease in Municipal bond maturities beginning in September

- All things being equal, this will help to alleviate downward pressure on yields with fewer maturity proceeds to reinvest

- Based on historical relative value observations, “AAA” MMD scale municipal yields are “rich” relative to comparable maturity Treasury yields across the yield curve

- They are currently below the average levels observed over a 30-year period at every point on the curve

Support for a Soft Landing: Consumer-Based

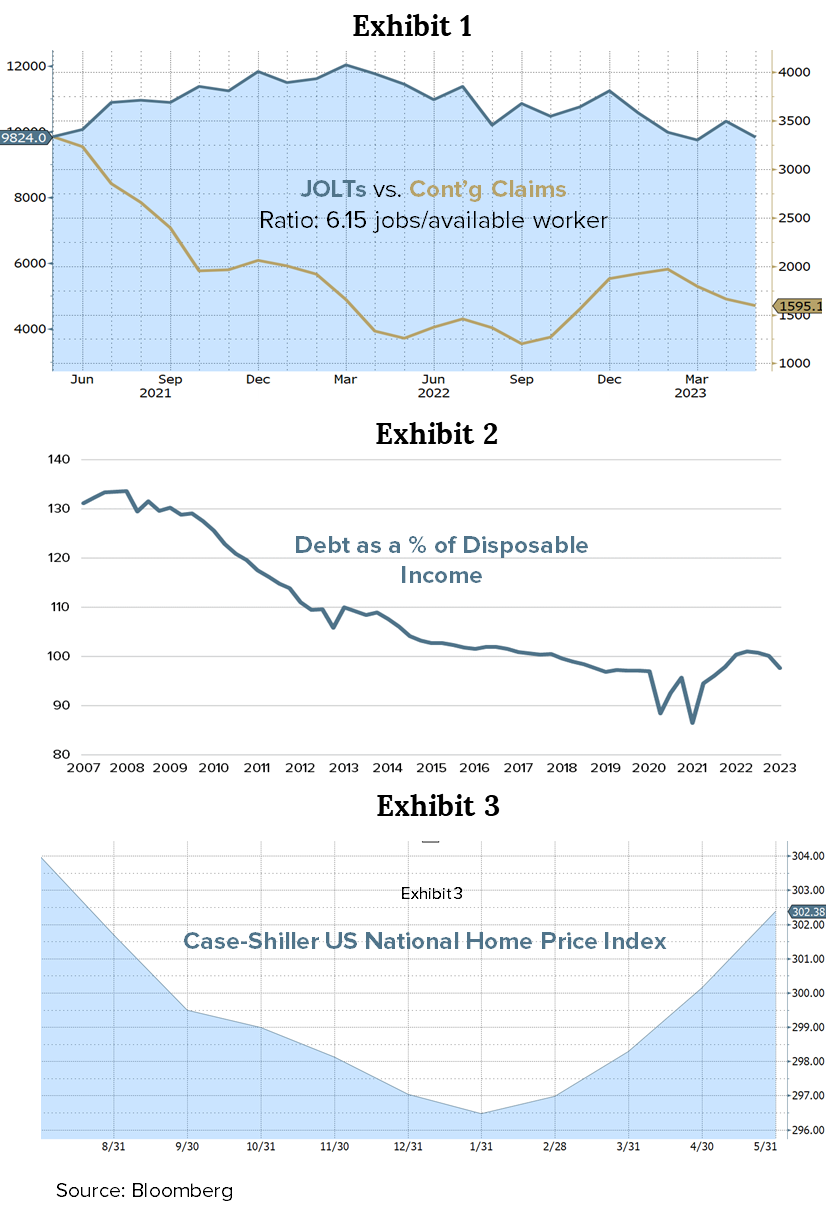

Conclusion: The U.S. is a consumer-driven economy and U.S. consumers are in very healthy financial shape, consequently, the lag between the onset of a Fed tightening campaign and a slowdown in demand appears to have lengthened.

- The persistent strength of the labor market supports consumption

- The Unemployment Rate and Job Openings to Available Labor Ratio (Exhibit 1) demonstrate this strength

- The lack of economic excesses, or sector bubble(s), does not encourage the need for (inevitability of) a correction

- Household finances remain strong after years of post-financial crisis healing and Federal COVID stimulus

- Excess household savings estimated to be over $1 Trillion

- U.S. effective interest rate on existing mortgage debt is roughly 3.55%; below the (pre-COVID) 2019 level of 3.87%

- Debt as a percent of disposable income is down roughly 30% from its 2008 peak (Exhibit 2)

- Housing market remains healthy

- The number of single-family units available is below 20+ year average

- Home prices are rising (Exhibit 3)

- The nature of the COVID inflation surge and the current well-anchored level of consumer inflation expectations supports the Fed's ability to pause (not overcorrect)

- Supply shock instigated inflation: self-correcting

- Consumer belief in the Fed's ability to cure inflation can influence actual inflation

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-148

September Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

November Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.

December Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.