Over its 10+ years of history, the Crawford Dividend Yield strategy has generated outperformance relative to its primary benchmark, the Russell 1000 Value Index. More significantly, the strategy has consistently provided superior results compared to the higher-yielding subset of the stock market. The strategy’s high level of dividend yield and proven security selection process are a result of our focus on finding longer-term investment opportunities that lie at the intersection of high quality and higher yield. From a portfolio perspective, we are differentiated by our strong total investment returns and the fact that we offer one of the highest-yielding actively managed equity strategies available to investors today. Our in-depth research process and longer time horizon enable us to identify investment opportunities that many investors overlook, ignore, or eschew due to shorter-term performance pressures and more myopic investment strategies.

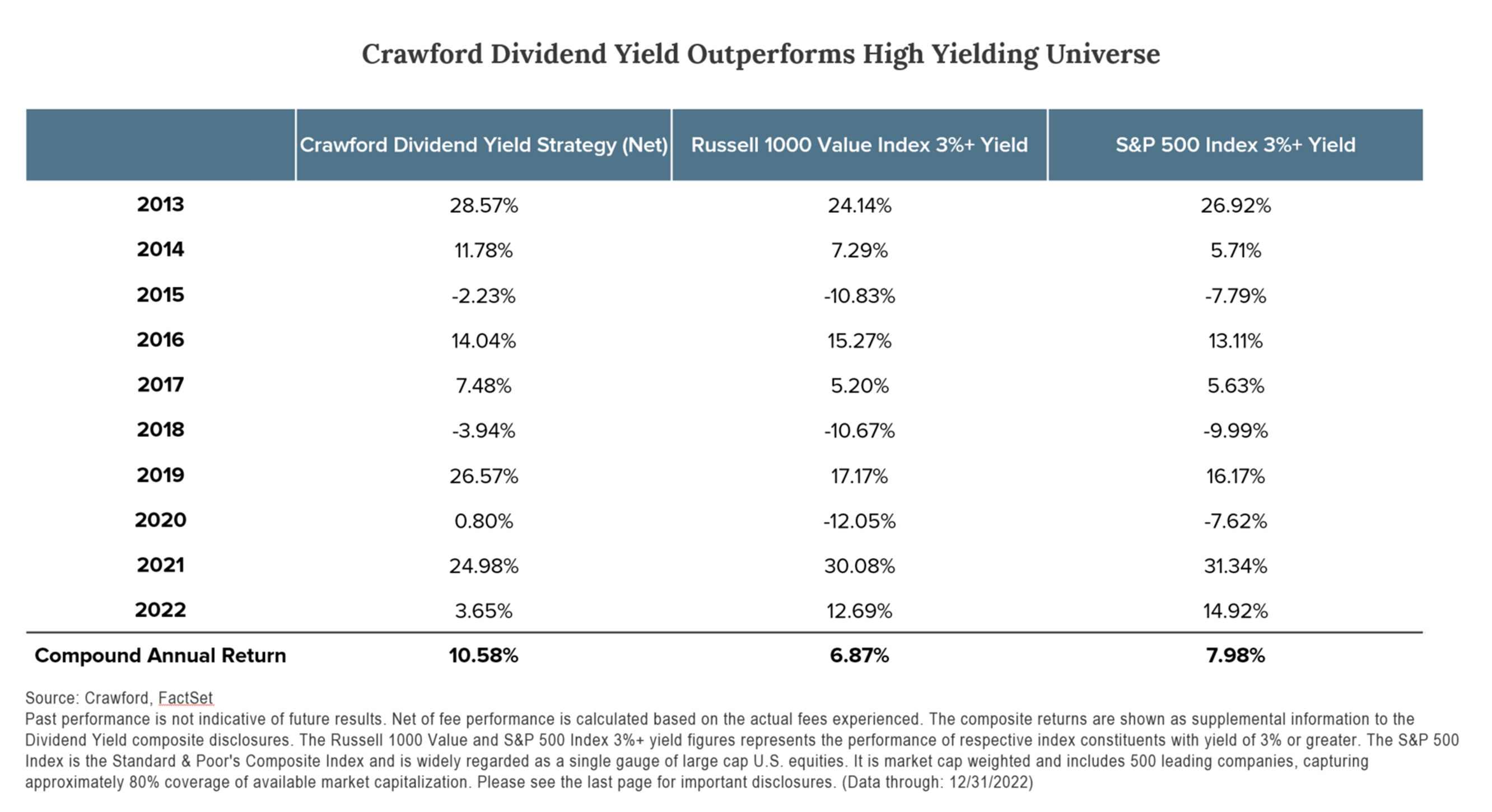

Because we are focused on higher-yielding stocks, our primary opportunity set for new investments is essentially stocks with yields of 3% or greater. In the table below, we have compared our results to higher-yielding stocks (3%+) in the strategy’s primary benchmark, the Russell 1000 Value Index, and those in the S&P 500 Index. In seven of the past ten years, the Crawford Dividend Yield strategy outperformed both of these higher-yielding opportunity sets, and the Crawford Dividend Yield strategy’s compound annual return over the ten year period is significantly higher. We believe this is reflective of the strength of our research process and our ability to identify attractive investment opportunities.

2021 and 2022 are the only years in the past decade in which the strategy underperformed both opportunity sets. For this two year period, primarily due to recessionary fears and the strength of the Energy sector, the higher-yielding area of the stock market outperformed the broader market. The Energy sector in the Russell 1000 Value Index was up a striking 56% in 2021 and 66% in 2022, and our strategy’s high-quality, diversified approach did not keep pace with the higher-yielding groups as investors demonstrated a preference for current income over future growth. Despite this, we believe our strategy’s results relative to the overall market were favorable, as the strategy kept pace with the Russell 1000 Value Index in 2021 and outperformed in 2022. Below, we highlight some of the components of our process that have contributed to our outperformance over time.

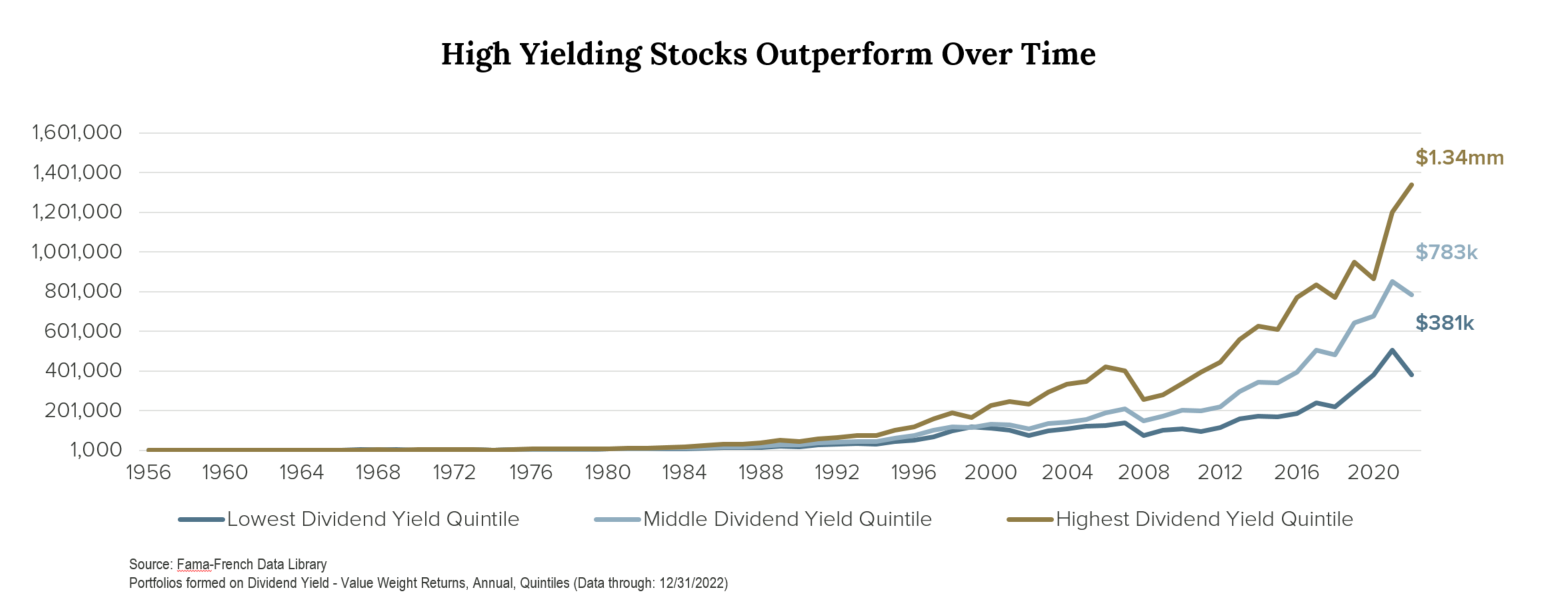

Long-Term Tailwinds: The strategy’s dividend yield has historically hovered at approximately 4%, and it is currently 4.45%. Contrary to common perception, we believe investing in the higher-yielding areas of the equity markets can provide a performance advantage. This belief is based on numerous academic studies that highlight the merits of investing in higher-yielding stocks, including those from Jeremy Siegel, Fama-French, and others.

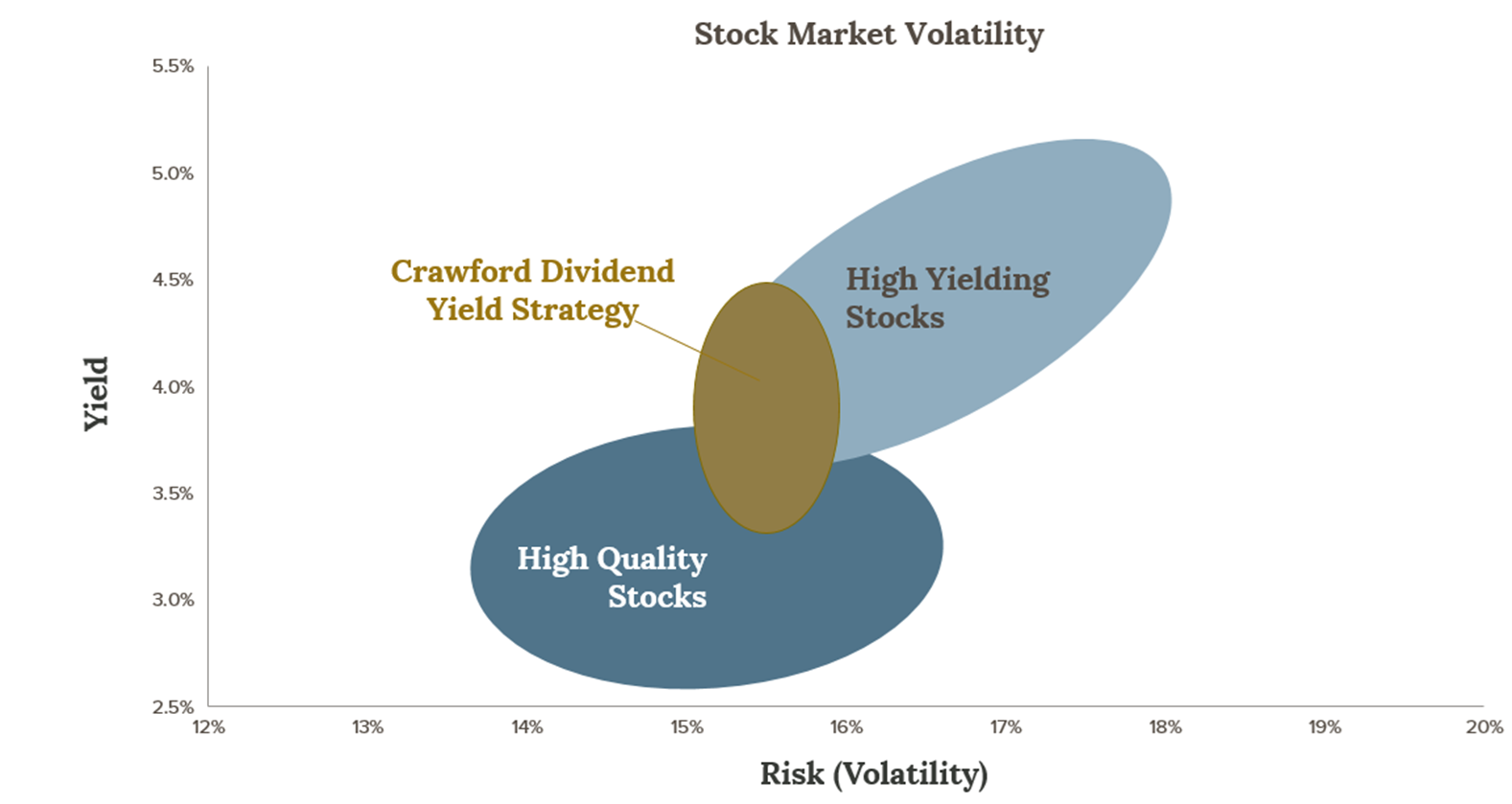

Avoidance of Dividend Hubris: We seek to benefit from the performance advantage of higher-yielding securities, but we deliberately manage the portfolio risk by keeping the yield below the highest area in the market (the 10th decile). We tend to buy more stocks in the 8th and 9th deciles because this is where we most typically find the optimal combination of quality and yield. By not investing in all of the highest-yielding stocks we are able to avoid Dividend Hubris. This phenomenon, where companies are paying an inordinately high dividend, puts the dividend and shareholders at risk.

Fundamental, Bottom-Up Research: Our analyst team of seven sector specialists applies rigorous, fundamental research to underwrite each security considered for purchase. We dig in to understand the company, its industry, and the competitive landscape. We analyze each of the financial statements to examine profitability, balance sheet strength, and cash flow generation/conversion. We scrutinize prior capital allocation decisions and assess management incentives and corporate governance to ascertain not just the ability and proclivity to sustain and pay the dividend, but also the ability to potentially grow the dividend over time. Holdings are re-evaluated at least quarterly (and when significant events occur) to evaluate progress in our thesis and assess the company’s Total Shareholder Return (TSR) prospects.

Diversification and Value-Orientation: Again, we combine high-yielding and high-quality stocks. The higher quality companies will typically have a lower dividend yield (albeit still above average) with stronger growth prospects, which contributes to the portfolio’s total investment return and in the process mitigates exposure to perceived “bond surrogates.” We also consciously seek diversification across sectors to provide broad market exposure. We do not do this just for diversification’s sake, but rather to widen our opportunity set to find more attractive value and TSR opportunities. This diversification also helps to dampen volatility and limit concentration in typical “yield” or “defensive” sectors. Our value approach is opportunistic by nature and enables us to move up and down the market capitalization spectrum to identify the optimal combination of yield, quality, and value.

Low Risk: An added byproduct of our process and the high-quality nature of our portfolio is that the strategy is less volatile than the overall stock market and primary benchmark. We also actively manage interest rate risk in the portfolio by monitoring exposures and company-specific business drivers. Many perceive most or all higher-yielding stocks as interest rate sensitive, but we have found a way to actively offset interest rate risk through our investment analysis and decisions. As a result, the portfolio has a demonstrated ability to preserve capital in both down markets and during periods of rising interest rates. The investment performance in periods of rising interest rates is significant because this is what has been occurring for the past six quarters or so.

No particular strategy, however, can provide superior results in every year and any environment. We have experienced numerous periods when higher-yielding stocks are in or out of favor with market participants. Such has been the case thus far in 2023 when market performance has been driven by narrow breadth (few stocks), and dominated by low yield and non-dividend-paying equities. This follows 2022 performance when we were able to provide positive returns amidst a bear market and as yields on the 10-year Treasury bond surged from 1.5% to ~3.9%. We have again outperformed our opportunity set for the year-to-date period. Our ability to do this when higher-yielding stocks are out of favor only serves to reinforce our confidence in our ability to add value over time.

Over most time periods, the Crawford Dividend Yield strategy’s results have been strong on an absolute, relative, and risk-adjusted basis. The strategy has participated in rising markets and helped cushion and protect capital in declining markets. We think the strategy’s high yield, our bias toward quality and value, and our in-house research are important contributors to our success and ability to generate total investment returns. We like to remind our investors that the return pattern for the Crawford Dividend Yield strategy may not always follow that of the popular market averages. When the strategy is out of favor, we actively search for opportunities that market volatility may offer us. We know from experience these opportunities will bolster future returns, and in the meantime, we are afforded the ability to be patient as investors and enjoy the high levels of income provided by the strategy.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-146

The Total Shareholder Return Trifecta

We invest to achieve an investment trifecta by selecting stocks that provide our investors with all three components of total investment return: fundamental business progress or growth, dividend yield, and valuation improvement

Don't Be Fooled By Dividend Hubris

Not all dividend-payers possess Dividend Integrity, and some actually exhibit what we call Dividend Hubris.

The Golden Opportunity: Crawford Small Cap Strategy

We came to realize that the small cap area of the market might actually be the best place to reap the benefits of our long-held philosophy.