In recent months, we have written about Dividend Integrity and how it might be as important now as it has ever been. Given everything that is going on in the markets and economy, we believe it is pertinent to emphasize that Dividend Integrity is more than just a company’s ability to pay and raise a dividend over time. The concept of Dividend Integrity alludes to the other attractive underlying quality characteristics that dividend history can signal, such as earnings consistency, balance sheet strength, and profitability, among others. An important point is that not all dividend-payers possess Dividend Integrity, and some actually exhibit what we call Dividend Hubris. These are companies that pay dividends to the detriment of their corporation. While these companies may frequently offer high current income, Dividend Hubris should be avoided via fundamental research and analysis.

Hubris often indicates a loss of contact with reality and an overestimation of one's own competence, accomplishments, or capabilities. – Wikipedia, Hubris

Companies that exhibit Dividend Hubris pay dividends, but the dividend is actually a source of fundamental weakness or impairment. While the dividend can help narrow the range of investment outcomes and stabilize investment returns for many companies, a dividend reduction or omission is likely to lead to a much wider range of outcomes on the downside. Some companies have an artificially high dividend that the underlying business model cannot sustain over the long term. In fact, it is often the highest-yielding stocks, or those that reside in the 10th decile of yield, that exhibit Dividend Hubris. Others may continue to pay a dividend even though financial circumstances indicate it is not prudent or when the underlying business is under pressure or economically sensitive in a downturn. This is often a symptom of corporate pride, it is bad for the business, and even though they are receiving the dividend, it is ultimately very bad for shareholders.

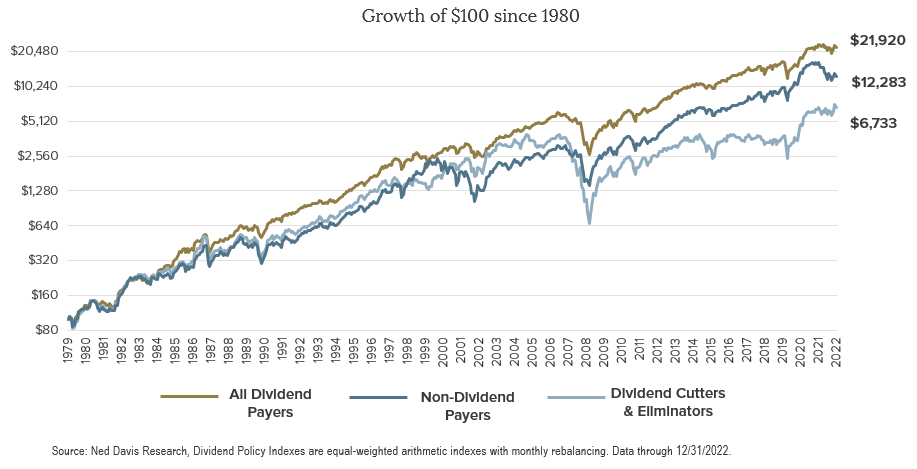

Companies that exhibit Dividend Hubris will eventually become dividend cutters & eliminators, a very bad place to be in terms of total shareholder return. The chart below demonstrates that this is the worst-performing subset of the overall stock market and also the most volatile category of stocks over time. In reality, the market often discounts a dividend cut a year or so prior to the company making a payout reduction or omission takes place. Thus, companies who cut their dividends underperform broader market averages, not only after they cut the dividend, but also leading up to the announcement as market participants begin to figure this out. This was outlined in a study conducted by Wolfe Research. Below, you can also see how dividend payers, and specifically those who exhibit integrity through maintaining and growing dividends, meaningfully distinguish themselves over time from both non-dividend payers and those that exhibit Hubris, or cutters/eliminators.

Discerning between Dividend Integrity and Dividend Hubris is where the importance of our fundamental, forward-looking, bottom-up research process and experience comes in. We start with the dividend as an initial quality screen, but we then analyze the business model, management strength, and company financials to determine whether or not the company can exhibit integrity over time. We invest for the long term and would prefer to miss an opportunity than invest in something we do not fully understand. In summary, our research process is complex, formal, diligent, and engineered to avoid companies with Dividend Hubris.

Investing in Dividend Integrity has been the primary way we have created successful outcomes on behalf of our clients, and we intend to continue to invest in this manner in the current market environment and in the years to come.

Please reference our related Podcast for more detail:

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Material presented has been derived from sources considered to be reliable, but the accuracy and completeness cannot be guaranteed.

CRA-23-149

Exploiting Inefficiencies to Produce Alpha: Crawford Dividend Yield Strategy

Over most time periods, the Crawford Dividend Yield strategy’s results have been strong on an absolute, relative, and risk-adjusted basis.

Dividend Integrity: Now More Than Ever!

Given the current environment, we believe now is a particularly good time to revisit and reemphasize our commitment Dividend Integrity.

The Dividend Effect

The Dividend Effect insulates investors from much of the volatility typically associated with investing.