A prevailing viewpoint in the investment community involves the belief that attractive businesses are growth focused. This means they dedicate the majority of corporate resources to expanding sales (and ultimately profit and cash flow) through investments in R&D, capital expenditures, and acquisitions. Conversely, companies that instead focus on returning significant amounts of capital to shareholders are often considered to be mature and lacking in growth prospects. At Crawford Investment Counsel (Crawford), we do not believe growth and return of capital are mutually exclusive.

Over our 42-year history, we have found that the most attractive investment opportunities are available in high-quality companies that succeed in investing for sustainable financial increase, while also returning substantial capital to shareholders through a steady and growing dividend. In many cases, these businesses also reduce the number of shares outstanding through periodic share repurchase. Crawford focuses on higher-quality companies that grow AND return capital to shareholders.

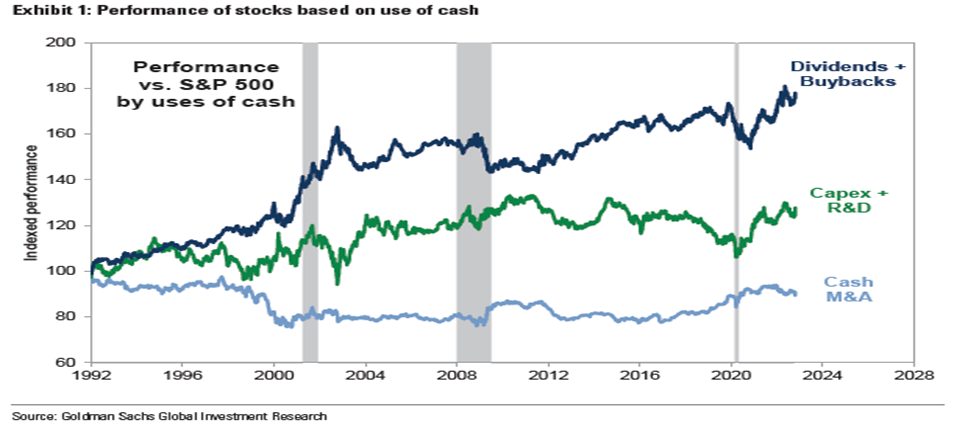

Contrary to the popular beliefs discussed above, the following chart illustrates that over the past 30 years, investors have actually demonstrated a preference for owning companies that devote most of their cash to dividends and share buybacks rather than indulging in growth-oriented spending on CapEx/R&D or M&A. Management teams are often incentivized (directly and indirectly) to pursue growth objectives, and this frequently yields low rates of return on their spending.

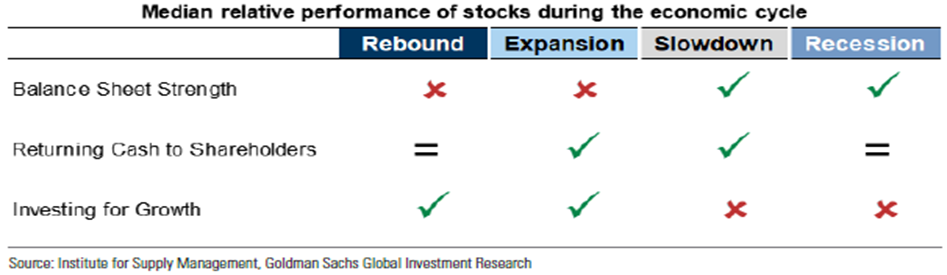

Investors’ capital allocation preferences will often vary based upon the perceived point in the economic cycle. However, in recent decades, businesses that are more focused on return of capital to shareholders have represented the most consistent path to relative investment outperformance throughout the economic cycle. Recessions are indicated in the grey vertical bars on the chart above. The table below illustrates that it is a superior business practice to return capital to shareholders in the lengthier periods of the economic cycle (expansion and slowdown) and remain at least neutral in the rebound and recession phases.

Dividends provide a steady stream of income that is highly valued by retirees. They also signal confidence related to a company’s ability to generate consistent cash flow in the future. Furthermore, dividends provide a steady call on firm cash flows, disciplining overall capital allocation. In most cases, dividend yield has historically been correlated with strong risk-adjusted returns. That is, over the long term, steady dividend payers usually win the race against volatile though sometimes extremely high returning non-dividend payers.

Share buybacks represent a more flexible form of capital return to shareholders. They can also create the potential for a lower risk and higher returning investment when deployed opportunistically at low valuations. In order to engage in value accretive capital allocation, businesses must ensure sufficient internal resources (strong balance sheet and cash flow stream) so they can act at the most effective points in the economic cycle and corporate life cycles. Companies with consistently well performing business models tend to naturally be in a superior position. These companies typically generate outperformance during periods of economic and equity market stress. Through investing in securities of this nature, Crawford strategies seek to generate reduced downside capture and preserve capital favorably in poor and more pedestrian market return environments.

Given changing economic circumstances, we believe the average company should generate more cash flow to reinvest for profit expansion or payout to shareholders. At Crawford, our investment strategies generate higher levels of cash flow, maintain strong balance sheets, and possess established track records of high payouts. We believe this balance amongst our portfolio constituents leads to a very high-quality mix of stocks that can provide attractive returns over a full economic and market cycle.

Please reference our related Podcast for more detail:

Disclosures:

There is no guarantee of the future performance of any Crawford portfolio.

This material is not financial advice or an offer to sell any product.

Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-22-270

Winning with Quality in the Consumer Discretionary Sector

At CIC, we seek high-quality companies for long-term investment.

Benefit of Working with CIC - Preservation of Capital

We consider preservation of capital to be a primary investment objective of any portfolio.

Living with the COVID Endemic

At Crawford Investment Counsel we are constantly working to stay informed and fully abreast of developments that can have an economic impact.