Let’s begin with some definitions for value and how these relate to investing.

Value: The regard that something is held to deserve; the importance, worth, or usefulness of something. (Source: Oxford Languages)

Value Investing: An investment strategy that involves picking stocks that appear to be trading for less than their intrinsic or book value. Value investors actively ferret out stocks they think the stock market is underestimating. They believe the market overreacts to good and bad news, resulting in stock price movements that do not correspond to a company's long-term fundamentals. The overreaction offers an opportunity to profit by buying stocks at discounted prices—on sale. (Source: Investopedia)

The Russell 1000® Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The Russell 1000® Value Index is constructed to provide a comprehensive and unbiased barometer for the large-cap value segment. The index is completely reconstituted annually to ensure new and growing equities are included and that the represented companies continue to reflect value characteristics. (Source: FTSE Russell)

The three definitions offered above go from conceptual and qualitative to 100% quantitative in an effort to ultimately capture a subset of the stock market that represents a value investment orientation. We wonder if something is not being lost in all this when it comes to index construction, for the resulting value indices are nuanced (if not flawed). For example, to arrive at the Russell 1000 Value Index, FTSE Russell (Russell) applies several conventions to the broader U.S. equity large cap universe. The use of price-to-book ratio as a primary indicator of cheap stocks is suboptimal and not nearly as relevant as it once was for various reasons. Furthermore, Russell utilizes lack of growth as a screening criterion. In our opinion, lower-growth companies do not necessarily suggest there is any existence of inherent value.

The methodology used by Russell to define index constituents leads many companies to be included in both growth and value indices. Russell’s indices are segmented by market capitalization, or size of companies, so the indices turn out to be both capitalization and characteristics weighted. These characteristics are related to relative measures of value and growth. Essentially, companies are split between growth and value characteristics based on price-to-book value and a blend of recent and projected earnings growth rates. This construction process is re-run each year and is not aligned with the way we, at Crawford Investment Counsel (Crawford), and most other price-sensitive or value-oriented managers think about investing today. This is due to two key reasons.

First, price-to-book ratio is not a primary barometer of most companies’ intrinsic values. Companies can and should trade above or below book value for good reasons. Changes to accounting rules and historical cost figures have made book value a largely irrelevant statistic for many businesses. Accounting conventions enable assets to be written down, and book value typically does not encompass intangible assets or brands, which can be a substantial portion of the worth of many businesses. Issuing stock or selling assets can result in an increase in book value, even if the company is worse off. Furthermore, assets can be owned off balance sheet, leases may or may not be capitalized, and historically goodwill has been amortized. In some industries, book value is a reasonably good measure of company worth, but in the majority of businesses, price-to-book ratio is a relatively weak and unimportant indicator of corporate value.

Earnings growth, the other measure on which Russell constructs its benchmarks, also does not necessarily imply value. Companies that have not been growing or will not grow in the future may or may not represent value as it relates to share price. Both utilizing book value as a primary indicator and including only slower or no-growth businesses leads to a suboptimal benchmark that is manipulated by construction rules. We wonder why anyone would find it compelling to invest in a strategy based on a simple combination of low price-to-book ratio and low growth. To us, it also doesn’t make sense that stocks would be included in both growth and value indices.

At Crawford, we employ an objectives-based approach to investing that we believe aligns better with both underlying corporate value and common sense. We are price-sensitive investors who believe the point at which an investor enters into a position has significant influence on the success or failure of any investment. But, we seek growing enterprises that demonstrate fundamental progress year in and year out. The dividend is our initial screening criteria, and we seek consistency and growth as a window into high-quality businesses that produce sustainable cash flows. This leads us to more predictable and consistent companies where we believe our likelihood of success is higher and the potential range of outcomes is narrower. We find value in reasonably priced and growing businesses where consistency is high and fundamental improvement is very probable.

Our process focuses on valuation, not as defined by Russell, but rather as defined by buying very high-quality companies when the market seems to be overlooking their financial strength, profitability, and underlying business consistency. This can happen for a number of reasons, but most typically it occurs when there is a shorter-term disruption in a company’s fundamentals and the share price declines to a greater degree than the underlying business’ value. For dividend-paying companies, this increases the yield and creates a valuation opportunity as fundamentals and price revert back toward mean levels. Importantly, our focus on dividends orients us toward those investments where the companies have the financial wherewithal to manage through difficult conditions. An added bonus is that we get to take the dividends home while we wait for fundamentals to improve. In summary, we seek attractive valuations relative to underlying business fundamentals.

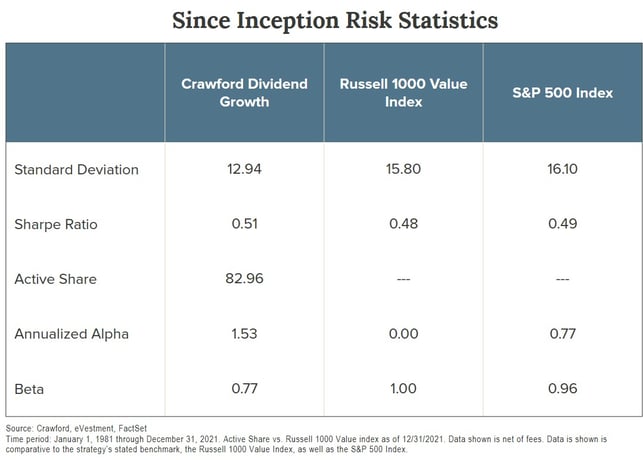

Since we utilize a different lens to identify value, the majority of our Dividend Growth strategy is not included in the Russell 1000 Value Index. Our active share figure of 83% is evidence of this. This means our strategy doesn’t really look or act like the index and as a result, produces very different, but what we believe to be, superior outcomes. The risk is materially lower and alpha highly positive compared to both the Russell 1000 Value Index and the S&P 500 Index.

Crawford has an investment philosophy that lies at the intersection of quality and valuation. We believe ours is a stronger portfolio construction process, which ultimately leads to positive alpha generation. However, it doesn’t outperform the index or primary benchmark each year due to tracking error and changing preferences within the markets. The overall level of market returns tends to have a major influence on relative manager performance, and higher return environments represent greater challenges for lower beta managers. With 20% less risk than the major market indices, even a semi-efficient market that is appreciating double digits becomes a difficult hurdle for higher-quality companies. Our since-inception alpha is significantly positive, which means we perform better than expectations would suggest, given our risk profile. Additionally, more recent performance has been favorable despite the robust return environment.

Going back to the formal definitions of value we outlined at the beginning, we believe the true value of anything is subjective and is ultimately in the eye of the beholder. At Crawford, we have a time-tested framework that identifies what we believe to be very good companies selling at reasonable prices. This formula has worked for us and our investors for over 40 years, and we expect it will continue to do so in the future, particularly as uncertainty is both pervasive and on the rise.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

There is no guarantee of the future performance of any Crawford portfolio. This material is not financial advice or an offer to sell any product. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The investment strategy or strategies discussed may not be suitable for all investors. Investors must make their own decisions based on their specific investment objectives and financial circumstances.

The widely recognized benchmark(s) in this presentation are used for comparative purposes only. The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower expected growth values. The S&P 500 Index is the Standard & Poor's Composite Index and is widely regarded as a single gauge of large-cap U.S. equities. It is market-cap weighted and includes 500 leading companies, capturing approximately 80% coverage of available market capitalization. The volatility (beta) of the portfolios may be greater or less than the benchmarks. It is not possible to invest directly in these indices.

CRA-22-084

Terminal Value: A Lesson in Asymmetry

We believe that at the forefront of any investor’s mind should be both the threat of principal erosion or permanent loss of capital and the significance of the pattern of their investment returns.

You Are Here: Intersection of Quality and Value

Crawford seeks to be at the intersection of value and quality. Here is how we get there.

The Intersection of Quality and Valuation

Valuation is an important and final component of our expected Total Shareholder Return (TSR) framework.