High inflation remains as the number one economic problem, not only in this country, but globally as well. It holds the attention of stock and bond investors, business owners, consumers, and of course, the Federal Reserve (Fed). In this article we will review recent inflation data and the implications for success in the fight to reduce inflation to acceptable levels.

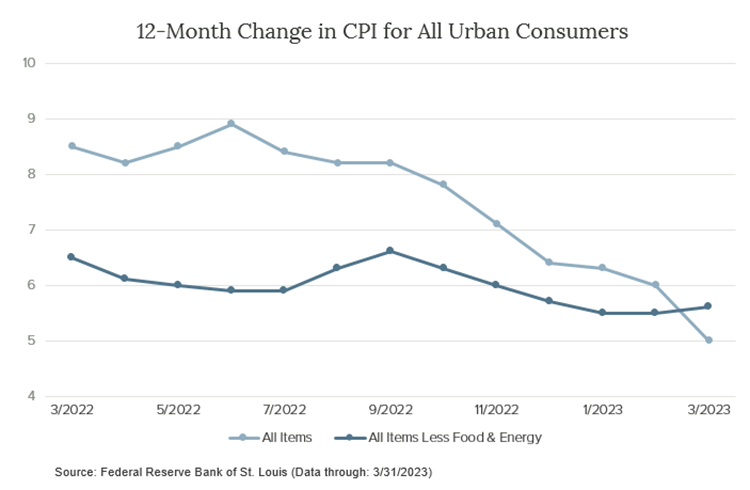

The Fed has established a goal of 2% for inflation. In March, the Consumer Price Index (CPI) had increased at a rate of 5% compared to March 2022. This represents a sizable drop from the February number which was 6.0%. During March there was barely any inflation at all as the month-over-month number came in at 0.1%. Even though inflation has dropped from a peak of 9%, we are a still a long way from the 2% target. Nevertheless, the progress made thus far is encouraging. And with some large monthly inflation numbers to compare to last year, the next few months may see further sizeable drops. We hope so.

While the CPI, commonly called the headline index, is the most widely cited measure of inflation, of perhaps equal importance is the CPI core index. The core index attempts to provide a more accurate measure of the underlying inflation rate by excluding the categories of Food and Energy. These are excluded because they are so volatile and tend to obscure the true picture of inflation. Now, here is the bad news. In March, the core rate actually accelerated, increasing 0.4% for the month and 5.6% year-over-year. The fact that the core rate is higher than the headline number indicates that underlying inflation is still sticky. The chart below illustrates the path of these two indexes.

One of the main reasons core is declining more slowly from its peak is because of the category of Shelter. Shelter reflects both renter and owner inflation and represents some 40% of the core index. This is by far the heaviest weight of any category, and it has been rising rapidly. In March, Shelter increased by 8.0%, a very fast rate. But recent Shelter patterns have been more encouraging and should filter into lower Shelter inflation in coming months. Nevertheless, CPI core is not making as much progress as expected, and this is concerning. The core number is also higher due to the absence of energy inflation, which has been in a declining trend of late.

We also note that the message from the Personal Consumption Expenditures price index (PCE), which is the Fed's preferred measure of inflation, is also pointing toward sticky inflation. On a year-over-year basis, PCE is running at 4.2% but PCE core is 4.6%. The conclusion: progress has been made, but there is more work to be done, and the 2% target is still a good ways off.

COMMENTARY. Much uncertainty surrounds the question of inflation, the Fed’s efforts to control it, and the timing and result of the eventual outcome. As a matter of perspective, we offer our thoughts on the likely resolution of some of this uncertainty.

We believe the Fed will persevere. Some doubt the Fed’s resolve; we don’t. The reputation of the Fed is on the line, and having admittedly made some mistakes on the front end of the inflation surge, we doubt they will err on the side of ease. Overdoing monetary restraint could lead to a recession, but even so, the Fed considers inflation to be a greater and more difficult problem to solve than recession, so we expect them to continue the fight against inflation with resolve.

We expect the Fed to ultimately be successful in achieving their target of 2% inflation. This is by no means an easy call, but our position is buttressed by the foregoing mention of the Fed’s resolve, plus two other factors that we believe are working in their favor. First, the supply disruptions that were such heavy contributors to inflation have largely been eliminated. This should make the path downward on inflation easier. Second, inflation expectations remain well anchored. The importance of this lies in the fact that consumers and forecasters believe the Fed will be successful and indicates that inflation is not deeply rooted. Consider, for instance, the inflation of the late 1970’s and early 1980’s. In that time, there was a two-decade buildup of inflation that caused most observers to believe that high inflation would continue well into the future. The result was that it took extremely stringent measures to correct the problem. This time, with lower expectations, the task may be easier.

Our optimistic view of the eventual outcome does not come without apprehensions. We are well aware of how difficult it is to unseat high inflation. Nor do we like the idea of a recession, if, in fact, that is what is required to solve the inflation problem. Realistically, a lot of work lies ahead to get inflation under control. However, from an economic point of view, it is essential that the inflation problem be solved. Inflation affects every person in the economy, destroys purchasing power, reduces wealth, impedes forward planning, and damages confidence. It is a bad thing, and the economic imperative is to reduce it in order to restore a more balanced, healthy, and more productive economy for all of its participants.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-093

The Psychology of Inflation

We believe that the psychology of both inflation amongst consumers and wages amongst workers will be key determinants of future inflation.

Inflation Update: Keep an Eye on Velocity

The inflation debate is front and center right now in the financial markets.

Crawford Bond Policy Update

Crawford's bond policy reflects the firm's stance on the fixed income markets, interest rates, inflation, and more.