It is important to distinguish among income, yield, and total investment return. Portfolio income is simply the dollar amount of stock dividends and bond interest payments expected to be received over the next 12 months. When this income figure is expressed as a percentage of the portfolio market value, it provides the yield (% rate). The income is what can be spent before invading principal, and it is a component of total investment return. The total investment return combines portfolio income plus or minus any capital appreciation or depreciation. The income is the stable component of this equation, so we want to emphasize it to the extent possible, but we report our results on the basis of total investment return.

In good times, the income component will be a smaller percentage of total investment return. In bad times, it may be all the investor receives. So while income is a critical component, short-term moves in share prices will typically dwarf the income component of return. We have a dual focus on both components of return, and we seek to earn attractive results through a combination of income and capital appreciation. It is the compounding of market value that enables our clients to enjoy the long-term benefits of our investment portfolios.

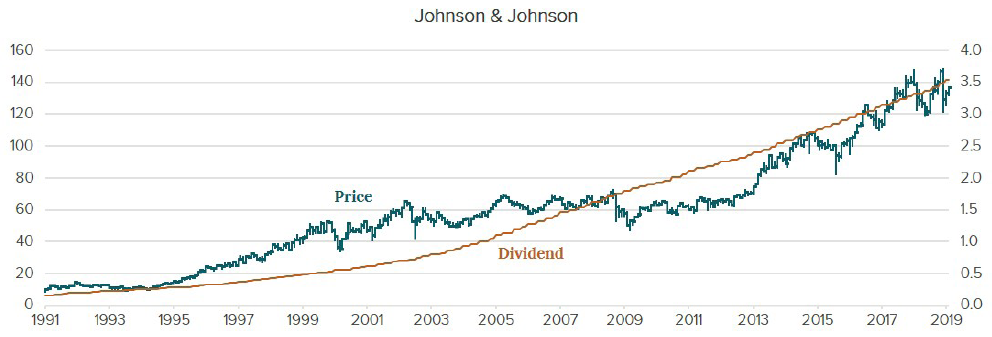

We believe one of the best and most predictable ways of producing an attractive total investment return is to focus on the dividend. One of the fundamental tenets of our investment approach is our long-held belief that a rising stream of income from dividends will be reflected in a rising share price over time. Income is one factor that gives value to stocks, so we focus on companies that can consistently pay and increase their dividends. See in the following chart how consistently the price of Johnson & Johnson stock follows the increase in the dividend line. The relationship between dividend income and price appreciation is not always as precise as in this example, but over the longer term the two are almost always positively correlated.

While compounding total investment return at an attractive rate is the end goal, we also seek to smooth the pattern of returns in the interim. This is important because it does not subject clients to excess volatility, helps avoid the asymmetry of capital appreciation or depreciation, provides a better chance of maintaining spending rates, and provides an overall higher comfort level for our clients. The best way to smooth out returns is to own high-quality bonds. The consistency of the companies in which we invest also helps mitigate risk and reduces volatility but still exposes the portfolio to the long-run benefits of equity ownership.

Crawford Investment Counsel is proud of the total investment returns we have been able to generate for our clients over four decades, and the fact that we have achieved these returns with much less volatility provides important benefits for our clients. The byproduct of more predictability is slightly less return when the market goes up, but downside protection when the market declines. This is a trade-off we are very willing to make, and depending on where we are in the economic/market cycle, our total investment returns may be above or below market indices that have varying investment characteristics that typically don’t align well with the needs of our clients.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request. Past performance is not indicative of future results. All investments carry a certain degree of risk of loss, and there is no assurance that an investment will provide positive performance over any period of time. This material is distributed for informational purposes only. The statements contained herein reflect opinions, estimates and projections of Crawford as of the date hereof, and are subject to change without notice. Forecasts, estimates, and certain information contained in this commentary are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Any projections herein are provided by Crawford as an indicator of the direction Crawford’s professional staff believes the markets will move, but Crawford makes no representation such projections will come to pass. Crawford makes every effort to ensure the contents have been compiled or derived from sources believed reliable, and contain information and opinions that are accurate and complete; however, Crawford makes no representation or warranty, express or implied, in respect thereof; takes no responsibility for any errors that may be contained herein or omissions; and accepts no liability whatsoever for any loss arising from any use of or reliance on this report or its contents. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or individual portfolio needs.

CRA-21-009

What’s up with GameStop?

Anyone with even a passing interest in the stock market is aware of the GameStop saga that is going on in the market.

Charitable Trusts: Doing Well While Doing Good

We believe our investment philosophy, focused on consistent income, long-term growth, and preserving capital, is well suited for the management of CRTs.

When Will the Fed Move?

There is great anticipation among investors as to when they will resume downward moves.