We consider preservation of capital to be a primary investment objective of any portfolio. The outcome we are seeking to avoid for our clients is the permanent loss of capital. We do this by incorporating a number of long-practiced disciplines into our portfolio management, security selection, and client-interfacing framework. Each step of our process seeks to help control risk. First, we include diversification by asset category, owning high-quality, income-producing securities. Second, we utilize a price-sensitive security selection methodology in the portfolio construction process, underwriting each and every investment decision to the best of our ability. Finally, we gauge and monitor a client’s risk and return tolerance and objectives through communication to ensure the portfolio is positioned to best meet the goals of each client. Each of these elements has been refined over the past 40 years of working with investors.

From time to time, market volatility may temporarily depress portfolio value, and individual stocks may be sold after a negative return, but this is different than a permanent loss of capital for the portfolio. High-quality securities, an approach that is diversified yet not “over-diversified,” a balance between risk and return, and a long-term orientation are all ways to help mitigate fluctuations in portfolio value. Conversely, a permanent loss of capital can occur when a portfolio declines beyond its recoverable value and is liquidated. This happens when a client is forced to re-evaluate and modify portfolio priorities toward safer categories in a market decline (abandonment or partial abandonment). This can also occur when excessive income needs are such that spending during a downturn forces sales that do not enable a portfolio to recover to its prior market value. Each is to be avoided, and our track record of success in this area is exceedingly high.

We believe diversification is one of the best risk management options available to investors. Sometimes described as a “free lunch,” the blending of asset categories can lead to higher returns with a smoother pattern of results (less risk or volatility). Our long-held belief is that stocks are the asset of preference and that high-quality bonds are the single best diversifier of equity risk. Downturns in the stock market are the reason to diversify, and it is in these periods that the correlation of high-quality bonds typically goes negative, meaning bonds are appreciating when stocks are declining. At the same time, most other riskier asset categories are experiencing ever higher correlations with stocks. Said another way, risk assets are highly correlated on the downside, but high-quality bonds are the one category that helps stabilize values. They can actually increase in value in times when investors need it most. Bonds are the best tool to help avoid a permanent loss of capital.

Our firm is extremely well-resourced from a research and analysis standpoint. In addition, we feel that we have the experience and perspective that can only be gained by working in the capital markets for decades. Along with a proper alignment of incentives, this combination greatly improves our clients’ chances for success. Because our efforts are highly focused on reduced volatility including down market protection, we believe we are better equipped to provide preservation of capital, which is the primary objective of many of our investors. The overall philosophy we bring to the investment equation is that investing is risky, so we seek to narrow the range of outcomes, improving the likelihood of success and helping to avoid adverse outcomes in the process.

We believe the best way to narrow the range of outcomes is to own high-quality securities. Quality is an important and often underappreciated investment characteristic. Quality is a driver of both risk and return. When paired with a value-sensitive selection process and effective portfolio management, it brings an element of defense to the portfolio. Our historical experience is that clients are shielded and experience increasing relative returns as a market decline accelerates. Our portfolios are engineered so that if a market decline becomes more severe, our clients’ portfolio values go down by a smaller percentage than the market averages. This is, in some part, due to the quality characteristic that we emphasize in individual security holdings. Quality is your friend in a market decline. There are many other attractive side-benefits to owning high-quality securities, including the fact that most produce income.

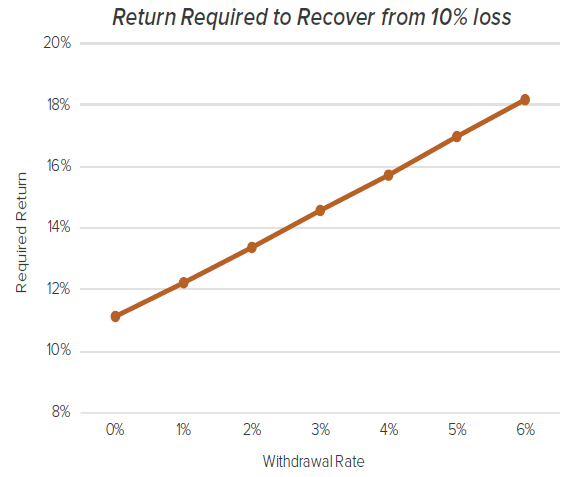

Income generation is an important safeguard and helps preserve capital. The distinction between total return and income is addressed, but having a spendable income stream can insulate investors from portfolio volatility, even if the portfolio yield does not cover 100% of current spending needs. Simply stated, the return of income is positive in each and every year. Market returns are variable, going up in most years but declining a not insignificant amount of the time. Conversely, portfolios managed by Crawford Investment Counsel seek to achieve rising income through growth of dividends in virtually each and every year. A significant level of growing income supports spending needs. This enables clients to adopt a longer-term perspective and limits the time required to recover market value after an inevitable market decline. The illustration below highlights the significant impact withdrawals have on a portfolio’s ability to recover losses. After a 10% loss, the portfolio will need to generate a return of 11.1% to break even. After a 10% loss and a 5% withdrawal, the portfolio will need to generate a 17.0% return to reach prior levels.

It is also critical that we fully understand and properly define a client’s risk tolerance. With this in mind, assets are allocated strategically and, to a much-lesser degree, based on conditions in the capital markets. This process of gauging and monitoring overall client circumstances and effectively balancing risk and return in any portfolio asset mix is a key value-add. There is risk in not taking any risk, but we know that the risk of exposing our investors to an overly aggressive program is most frequently learned once it is too late. We would rather miss out on some return and experience an opportunity cost in up markets than realize after the fact that a program was misaligned to navigate down markets, the result of which could be permanent impairment.

We continually monitor client needs and look for changes in individual circumstances that could necessitate a shift in investment policy. Communication is key, for communication is the best way to avoid misalignment which can, in turn, lead to the abandonment of an investment program. This risk of abandonment is underappreciated and almost never occurs at an opportune time. Moving to a less-risky allocation after the market declines (but before it recovers), shifting to an aggressive strategy late in the cycle, or chasing higher returns after the market has already gone up are all symptomatic of abandonment and are most typically not in anyone’s best interest. Simply put, market volatility often makes investors do what they shouldn’t, leading to a loss or impairment. The attributes we have described as central to our approach help reduce the likelihood of this occurring. Our goal is to honor the objective of preservation of capital and keep the focus on the longer term, which, in turn, enables one to enjoy the benefits of a compounding that comes with a consistently employed investment program.

Disclosures:

Crawford Investment Counsel Inc.(“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request. Past performance is not indicative of future results. All investments carry a certain degree of risk of loss, and there is no assurance that an investment will provide positive performance over any period of time. This material is distributed for informational purposes only. The statements contained herein reflect opinions, estimates and projections of Crawford as of the date hereof, and are subject to change without notice. Forecasts, estimates, and certain information contained in this commentary are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Any projections herein are provided by Crawford as an indicator of the direction Crawford’s professional staff believes the markets will move, but Crawford makes no representation such projections will come to pass. Crawford makes every effort to ensure the contents have been compiled or derived from sources believed reliable, and contain information and opinions that are accurate and complete; however, Crawford makes no representation or warranty, express or implied, in respect thereof; takes no responsibility for any errors that may be contained herein or omissions; and accepts no liability whatsoever for any loss arising from any use of or reliance on this report or its contents. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or individual portfolio needs.

CRA-21-009

Benefit of Working with CIC - Income and Growth of Income

Owning income-producing securities is an important and differentiating element of working with Crawford Investment Counsel.

Tariffs & Turbulence: Why Quality Counts

Considering the potential effects of tariffs only serves to underscore the importance of our fundamental, bottom-up research process and high level of scrutiny in our company due diligence and investment decision-making process.

Charitable Trusts: Doing Well While Doing Good

We believe our investment philosophy, focused on consistent income, long-term growth, and preserving capital, is well suited for the management of CRTs.