The Federal Government again hit the $31.4 trillion debt ceiling on January 19, 2023. This forced Treasury Secretary Yellen to begin implementing “extraordinary measures” to ensure the government has enough cash and does not go into default. If it seems like we have been here before, we have.

The debt ceiling was created by the Liberty Bond Act of 1917. Since that time, the debt ceiling has been raised 90 times, including 78 times since 1960 (i.e. more than once a year): 49 times by republican presidents and 29 times by democratic presidents. There have been ten occasions since 1980 when the debt ceiling was not increased by the deadline, resulting in a partial Federal Government shutdown. Most of these were only for one or two days, but from December of 2018 to January of 2019, the Federal Government was in partial shutdown for 35 days.

“As reckless as a government shutdown is…an economic shutdown that results from default would be dramatically worse. And the United States is the center of the world economy. So if we screw up, everybody gets screwed up.”

~President Barack Obama, 2011

The projected deadline for a government shutdown is June 1, as tax receipts collected through April 15, 2023 were slightly lower than originally forecasted. Why should this be watched more closely than usual?

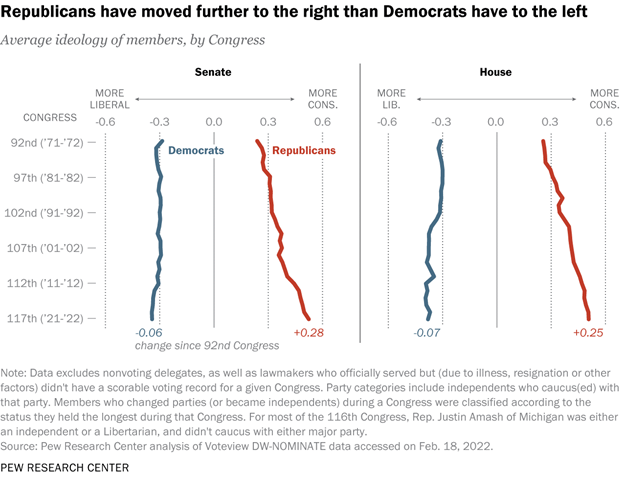

Partisanship is rampant. Partisanship is so rampant that it is difficult to find statistics that fairly show how divided our political leaders have become. The graph below from Pew Research, a non-partisan think tank, shows the split between the two parties. Both parties are so entrenched in their side that compromise is rarely found. The debt ceiling, which should be a non-partisan issue, is being held captive by both parties as leverage to achieve other partisan goals.

President Biden is using a similar tactic to President Obama in 2011, insisting the debt ceiling is “a matter of principle” and not a negotiation point. Ironically, the Obama presidency gave into negotiations for the debt ceiling in 2011, but then twice was able to increase the debt ceiling without negotiation. Biden’s current negotiating tactic combined with razor-thin margins held by the republican House and democratic Senate means that any small dissension in parties could result in shutdowns.

So what should investors expect?

Historically (since 1989), when the debt ceiling is increased, there has been very little impact on returns in financial markets, including debt, equity, or commodities. In the limited instances where the Federal Government has shut down, riskier assets tend to outperform after the debt ceiling has been increased, specifically the S&P 500 Index and emerging market equities. Although a very limited data set, credit rating agency events surrounding the debt ceiling are similar to but more impactful than a shutdown. These return patterns typically stabilize after about a month.

Markets have been showing some signs of concern. The T-Bill market is highly liquid and very stable, and thus very small moves in yield are often seen as warning signs for other markets. On April 20th, the spread between the one month and three month government T-Bills reached a peak of 180 basis points. Simply put, investors were willing to accept an annualized return of about 3.2% for lending the U.S. Government money for one month, but required close to a 5% annualized return to lend the U.S. Government money past the debt ceiling. Within two weeks, the premium in the currently offered one month T-Bill had disappeared, as it would need to be held through the debt ceiling deadline.

As we go to print on this Perspective, it is being reported that meetings are being set for a compromise to have a limited increase in the debt ceiling. This small increase would give both sides more time to come to a larger debt ceiling compromise.

We do not foresee a nightmare scenario - an inability to compromise such that the U.S. Government defaults on its debt. Several market pundits are offering up probabilities on this occurring, but we view that as uninformed speculation. Tail risk events, events with little probability of occurring that could have large potential consequences, are extremely hard to manage. This is because insurance or over-active management has a cost that, over time, outweighs any benefits of the once-in-a-lifetime catch.

We view companies with conservative balance sheets and durable cash flows as safeguards in this environment, especially companies with both global revenue and expense footprints. More importantly, these tail risk events often shake out the weakest hands, resulting in selling at the bottom and a permanent loss of capital. To avoid that for our clients, we focus on metrics that show the health of a business – dividend yield, free cash flow growth, market share gains – and take the mentality of long-term owners, not traders. At Crawford Investment Counsel, we have helped our clients survive the ups and downs of the market for over 40 years with high-quality, dividend-paying stocks as the backbone to their portfolios.

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-101

Stocks: Rent or Own?

Today, many are effectively “renting” stocks in an attempt to create short-term trading gains, rather than owning equities for long-term total investment return.

It's Easier Said Than Done

Many would be shocked to learn that the majority of common stocks have lifetime buy and hold returns that are less than that of one month Treasury Bills. Said differently, the stock market overall generates attractive long-term returns, but most stocks fail to even match the returns of Treasury Bills.

Introduction to Behavioral Investing

Crawford's investment philosophy is intentionally designed to work with, rather than against, human nature.