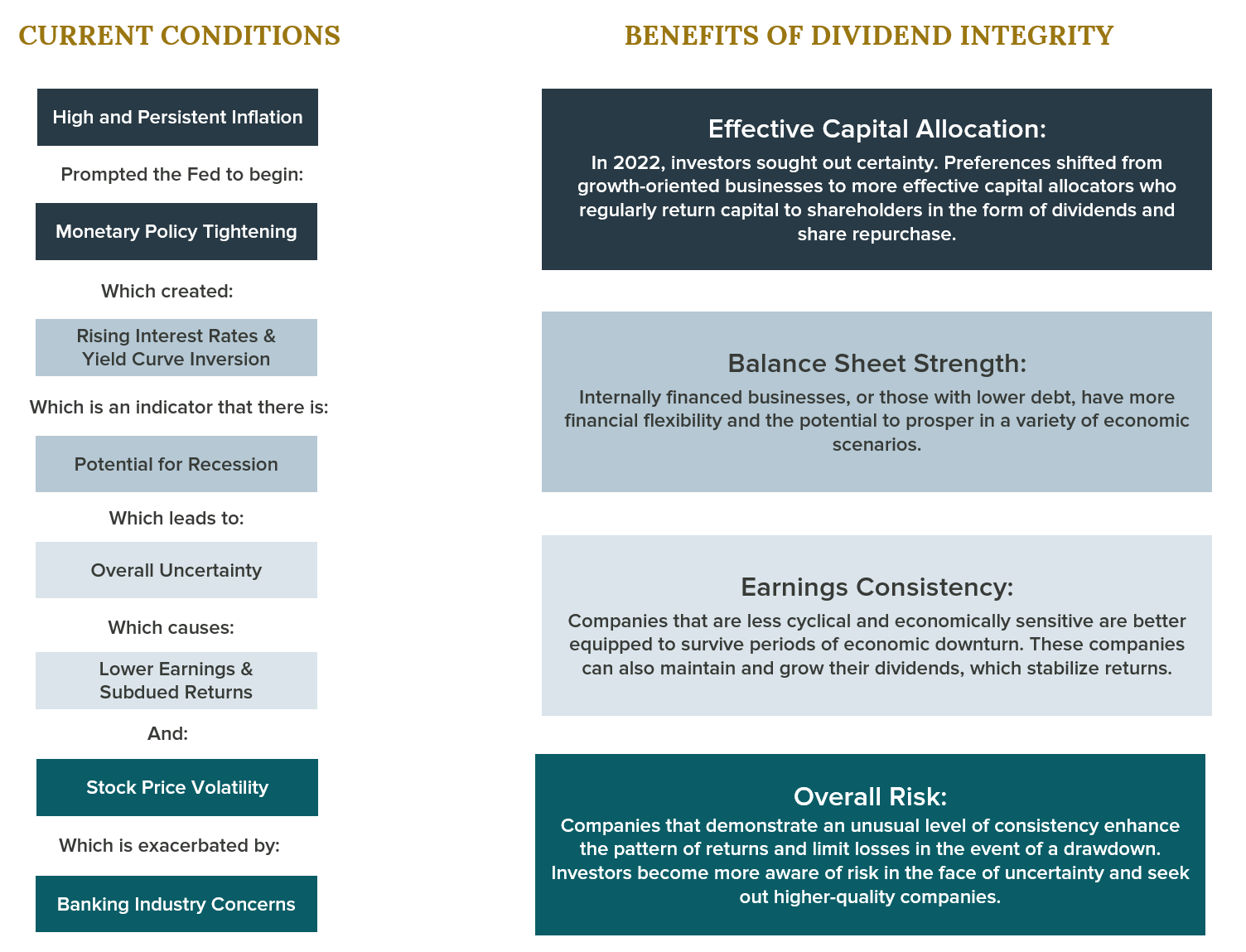

This update comes at a highly uncertain period for the economy and financial markets. The Federal Reserve (Fed) recently raised interest rates again to over 5% to combat persistent inflation, unemployment is at a very low level with a large amount of unfilled jobs, and just this year we have seen three of the four largest bank failures in our nation’s history. Most are anticipating a recession, but it is unclear when it will arrive, how severe it could be, and whether or not the Fed is completely done raising interest rates. We are also facing a potential debt ceiling crisis. Until more clarity around these issues is achieved and the fight against inflation is won, we expect to experience further fits of market volatility. Despite the uncertainty, we are confident that our focus on quality and Dividend Integrity will continue to be a favorable investment factor that can help portfolios weather a variety of economic and market outcomes.

The aforementioned issues represent some of the larger questions investors face today. Trying to predict all of the ultimate outcomes, along with the reaction of the capital markets, is a risky way to make investment decisions. Similarly, forecasting quarterly earnings with precision or attempting to determine the immediate future path of interest rates is very challenging. These are areas where it is difficult to achieve a persistent investment edge. For this reason, we invest with an approach that acknowledges the reality of uncertainty and focuses on investments with a higher likelihood of success. These investments have better visibility and a narrower range of outcomes, produce steady income, and demonstrate Dividend Integrity.

We define Dividend Integrity as simply the ability of a company to sustain and/or raise its dividends over time, consistently rewarding shareholders in the process. For us, dividends are considered an initial indicator of quality. Once this criterion is satisfied, we move forward in our fundamental research process with the belief that the ability of a business to regularly pay and sustain dividends is often indicative of quality characteristics like balance sheet strength, consistent cash flows, low earnings variability, and high return on equity. Secondary attributes often include strong management teams, substantial market share positions, a business with low capital requirements, and sound capital allocation practices. Here are some of the ways these favorable aspects can help sustain portfolios during periods of uncertainty:

Currently, we note that futures markets are estimating an end to federal funds tightening as early as this summer. However, we doubt the likelihood of this occurring. The economy, particularly the labor market, is too strong, and inflation, while it has declined from its peak, is too far from target and continues to remain sticky. These two factors seem to prohibit an early move toward easing. Our view is that some length of time is likely to pass before enough information is revealed about the economy, particularly inflation, to know for sure that it is safe to proceed toward easing.

With regard to the possibility of either recession or soft landing, indicators suggest the more likely outcome is recession. One of the historically reliable predictors of recession is an inverted yield curve, and the yield curve today is severely inverted. The lending and credit function in the economy is dependent on lenders borrowing short (at lower rates) and lending long (at higher rates). An inverted curve destroys this function and discourages lending, the grease that makes the economic wheel turn. We have been on recession watch for a number of months and we remain so, even though we do not go so far as to predict one.

While soft landings are the rare exception in tightening cycles, they are not totally unprecedented nor impossible to pull off. One fact that encourages us to consider the possibility of a soft landing is the current strength of the labor market. More than a year into the tightening phase, the unemployment rate is lower than it was pre-pandemic. At 3.4%, it is at a 50-year low. And of course, employment is the single most important factor in sustaining demand in the economy. If employment remains strong enough for long enough for inflation to begin a steeper descent toward target, it is possible that a soft landing will be achieved. Again, this would defy the odds, but it is not out of the realm of possibility.

Our view is that this uncertainty will eventually yield to more normal and balanced economic activity. Until that time arrives, our best efforts will be to bolster the quality and defensiveness of the portfolios as a buttress against the uncertainty and implied risk in the current economic setting. Once again, we remain committed to investing in companies that exhibit Dividend Integrity, and we search for an unusual amount of consistency and predictability in the face of uncertainty.

Disclosures:

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

CRA-23-103

Mid-Quarter Update - February 2023

The rising tide of optimism that was evident in January is being followed by a period of uncertainty around what is ultimately required for the Federal Reserve (Fed) to complete their work.

September 2024 | Quarterly Letter

We find ourselves at an inflection point in the economy. After more than two years of raising and holding the federal funds rate high, the Fed recently reduced that interest rate by 50 basis points.

March 2022 | Quarterly Letter

Of the many uncertainties we face, we believe the greatest is that which surrounds the potential outcome of the conflict between inflation and the Fed.