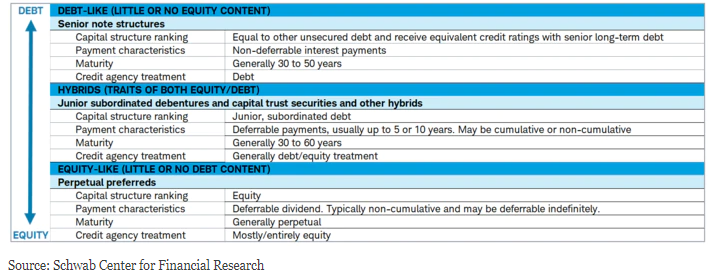

Preferred stocks are equity securities that are required to pay interest or dividends before common dividends are paid to common stockholders. This characteristic makes preferred stock senior to common stock, but junior to bonds or other debt carried by corporations. This seniority applies to distribution of cash flows (dividends) and liquidation in the event of bankruptcy. Major characteristics of preferred stocks include fixed or floating rate coupons, long maturities (many are perpetual or have five year call provisions), no voting rights, cumulative or non-cumulative dividends, and usually a credit rating.

Different Preferred Security Structures

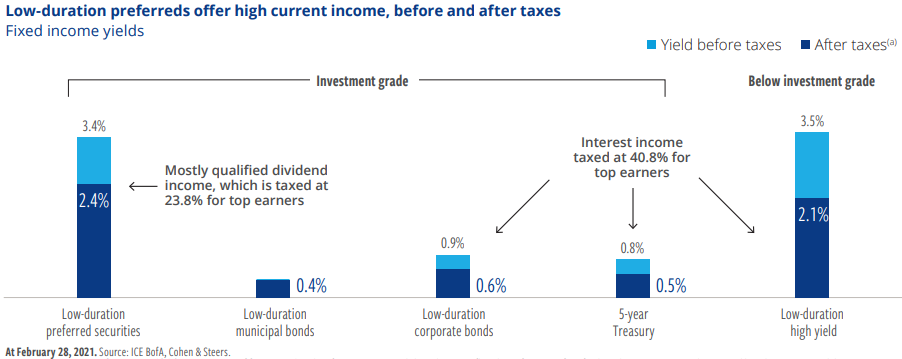

Preferred stock usually carries higher coupons or yields than common stock dividends and bonds of the issuing company. We believe this makes preferred stock an interesting option for yield-seeking investors. A key distinction of preferred stock versus bonds is their favorable tax treatment (excluding REIT preferreds). Illustrated below are the after-tax yields for qualified preferred dividends, which are taxed at 23.8% versus 40.8% for bonds. This creates almost as much as 2% incremental yield (200 basis points) in preferred stock versus various fixed income issues.

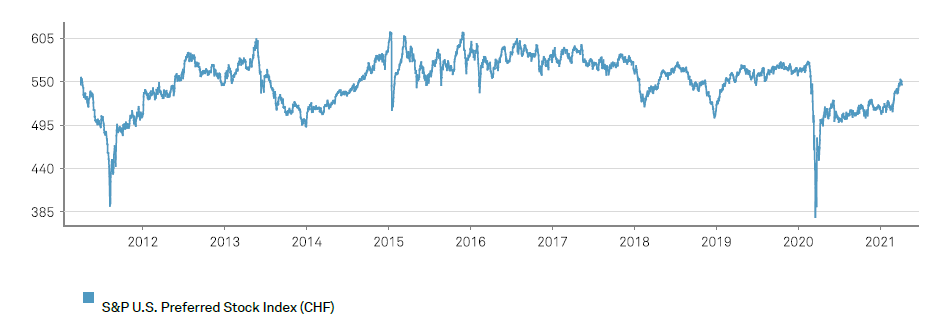

However, higher income also comes with different risks than bonds. Given that preferred stock is technically an equity security, its prices are more volatile than fixed income securities, especially during turbulent market events such as the beginning of the pandemic in March 2020. The S&P Preferred Stock Index shown in the chart below has regained most of the decline from 2020, but it was volatile.

Source: Source: S&P Dow Jones Indices, S&P U.S. Preferred Stock Index (CHF) Fact Sheet

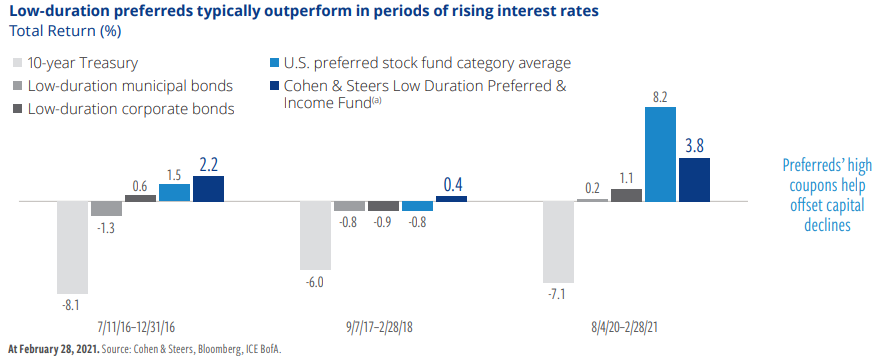

Another consideration is interest rate risk. Most preferred stocks have long maturities with fixed or floating rate coupons, which makes security selection very important in a rising interest rate environment. In order to limit interest rate or duration risk, adding fixed to floating rate or floating rate preferreds can moderate this risk. Shown below are the last three higher interest rate periods in which preferred stocks did not decline as much as one might have expected. According to Cohen and Steers, this is due to the higher coupons in preferreds and adding floating rate preferreds to dampen higher interest rate risk.

Preferred stock also carries some credit risk as the issuer is not contractually obligated to pay a preferred dividend unlike fixed income securities. However, as mentioned previously, the issuer must pay the preferred dividend before paying the common dividend, which creates a strong incentive to pay the preferred dividend.

Conclusion

We believe the favorable risk-adjusted income characteristics of preferred stock make this misunderstood security an optimal place to find higher income. At Crawford, we are active participants in owning and managing preferred securities within our Crawford Managed Income Strategy.

Disclosures:

Crawford Investment Counsel Inc. (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request.

This material is distributed for informational purposes only. The opinions expressed are those of Crawford. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Forward looking statements cannot be guaranteed.

CRA-21-137

Growth of Income: Two Paths, One Philosophy

Our Dividend Growth and Dividend Yield strategies offer two distinct paths to harness the power of dividends, allowing investors to align their portfolios with their specific income and return objectives.

Why Dividends Matter: Downside Protection

One of the more favorable aspects of investing in dividend-paying stocks is their ability to help protect capital in declining stock markets.

The Total Shareholder Return Trifecta

We invest to achieve an investment trifecta by selecting stocks that provide our investors with all three components of total investment return: fundamental business progress or growth, dividend yield, and valuation improvement