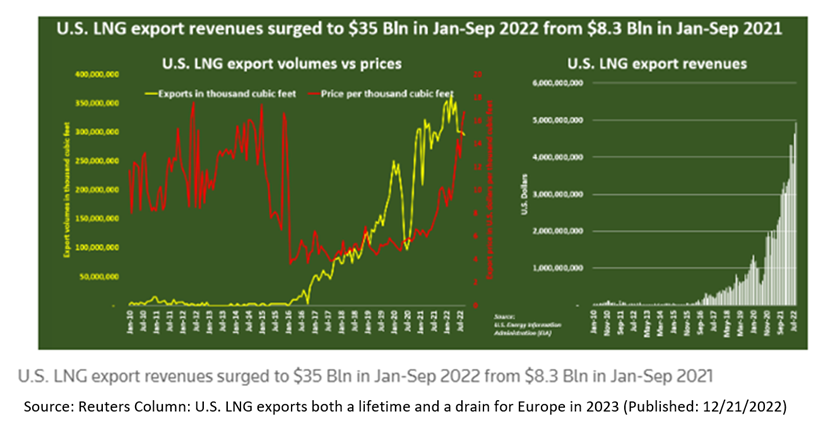

The United States began exporting Liquefied Natural Gas (LNG) from the Lower 48 in 2016. According to the EIA, as of July 2022, the U.S. has more LNG export capacity and has exported more LNG than any other country. U.S. LNG exports averaged 11.1 billion cubic feet per day (Bcf/d) during the first half of 2022. What caused the surge in demand for U.S. LNG exports?

The answer: Putin’s 2022 invasion of Ukraine and the weaponizing of Russia’s own natural gas exports to Europe. This “blunder” not only reduced capital inflows into Russia, but also forced European nations to find alternative sources of energy. What unfolded in 2022 and continues today is an LNG export boom for U.S. Energy and Energy Infrastructure companies.

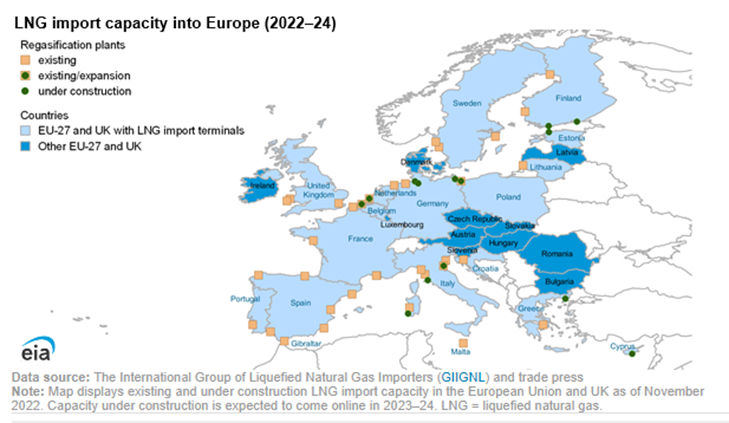

As a result of Russia’s war, European countries are quickly building new import capacity. LNG import capacity in the EU and UK will expand by 34%, or 6.8 Bcf/d, by 2024 compared to 2021, according to the International Group of Liquefied Natural Gas Importers (GIIGNL) and trade press data.

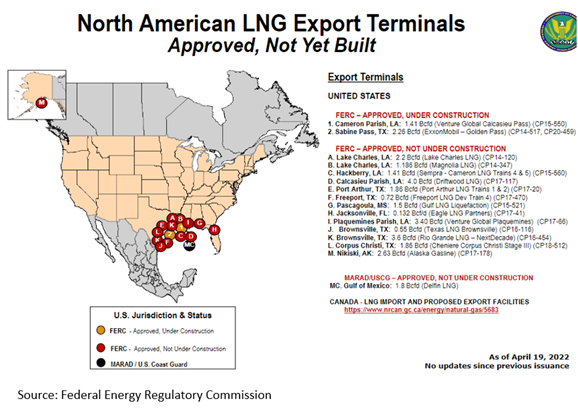

How is Crawford participating? U.S. LNG exports are only possible with energy infrastructure, which includes the pipelines, processing and gathering equipment, and storage terminals necessary to get natural gas to export markets. We are participating in this development through ownership of Williams Companies (WMB), Kinder Morgan (KMI), DT Midstream (DTM), and Oneok (OKE). These companies contribute to the backbone of U.S. energy dominance. In fact, it is highly likely that the natural gas being exported is running through the pipes of one of the aforementioned holdings.

There are currently thirteen approved U.S. LNG export projects not yet under construction. These projects will depend on the critical infrastructure of our holdings in the years ahead. We believe the prospects for these higher-yielding companies have never been brighter, courtesy of “Putin’s Blunder.”

Disclosures:

Crawford Investment Counsel (“Crawford”) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford, including our investment strategies, fees, and objectives, can be found in our Form ADV Part 2and/or Form CRS, which is available upon request.

The companies identified above are examples of a holding and is subject to change without notice. These companies have been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment recommendations or decisions we make in the future will be profitable.

The opinions expressed are those of Crawford. The opinions referenced are as of the date of the commentary and are subject to change, without notice, due to changes in the market or economic conditions and may not necessarily come to pass. There is no guarantee of the future performance of any Crawford portfolio. Crawford reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

CRA-23-042

Quality: A Silk Purse Out of a Slow World

The last decade aside, the world has been experiencing a long-term slowdown in growth rates.

The High-Grade Bond Market Today: Compressed Yields & Longer Duration

Since the Global Financial Crisis, changes in the U.S. high-grade bond market are exposing passive fixed income investors to a heightened level of risk.

The U.S. Remains a City on a Hill

U.S. exceptionalism, whether thought of in its broader original context, or the more restrictive financial and economic context, is essential to the future well being of our country.