The higher-yielding subsets of the capital markets tend to be dominated by income-seeking investors, the vast majority of whom are individuals. At Crawford Investment Counsel, our 40+ year history of investing in dividend stocks has taught us that when seeking yield, investors (and speculators) often must accept “something else” that comes along with the yield. These “something elses” are often misunderstood and underappreciated by individual investors and a number of their professional counterparts.

All of this means that certain higher-yielding areas of the capital markets can be inefficient opportunity sets, offering income and attractive returns to those who possess analytic and risk management advantages. At Crawford, our Managed Income Strategy generates attractive, income-oriented returns with lower risk by exploiting these opportunities in higher-yielding securities.

First, a review of the asset categories eligible for investment in the Managed Income Strategy. High dividend stocks, preferred stocks, corporate bonds, energy infrastructure companies, and REITs are owned in varying proportions to generate a target portfolio yield of 5-7% with the opportunity for capital appreciation and dividend increases. Each of these markets are nuanced and offer both opportunity and risk. Let’s review each one, examining the opportunities and how Crawford invests in these areas.

High Dividend Stocks: This is an area where Crawford has what we believe to be a core competency and proven record of successful investing. Our 10-year track record of investing in higher-yielding stocks has proven far superior to the opportunity set. Suffice it to say, there are opportunities for professional income investors to improve upon the returns offered by the higher-yielding segments of the stock market.

Preferred Stocks: We believe we add value through individual stock selection. The largest ETF that follows the preferred market is passive and represents approximately 5% of the market value of all outstanding issues. Many of the securities in this area are relatively small and often held to maturity. With 62% of the outstanding issues being banks and another 13% insurers, the financial industry exposure is extreme. We offer diversification and also possess a size advantage. Our ability to manage call risk, own qualified issues, select only those credits we find attractive, and own fixed-to-floating rate securities all add to our ability to out-maneuver the ETF. We have regularly observed securities trading at negative yield to call ratios, illustrating the illiquidity and lack of discretion of passive vehicles and investors. Preferred stocks are an attractive area for investment but become even more compelling as a component of a portfolio of various higher-yielding asset classes due to the concentration and dynamics of the marketplace.

Energy Infrastructure: C-corporation (C-corps) energy companies are the vehicle of preference here and offer advantages relative to MLPs. Our focus on C-corps can be attributed to a number of factors, the primary factor being to avoid complicated tax issues including annual K-1s that are produced by MLPs. The C-corps we own also have stronger governance policies. We feel that many MLPs have had a poor track record of governance, and in some cases, the alignment between management and investors can create conflicts. We seek out investment-grade companies with mission-critical assets, ample free cash flow, good balance sheets, and generous dividend yields.

Corporate Bonds: The corporate bond market is vast, and our ability to cherry pick issues, especially where our equity research team follows the stock, is, in our opinion, another embedded advantage. Our equity research analysts work closely with our fixed income team to arrive at a select group of higher-yielding corporate bonds which we believe offer an attractive risk/return tradeoff, specifically with regard to interest rates.

REITs: The ability to invest in real estate while benefitting from the liquidity of the stock market is an attractive feature of REITs. REITs benefit from secular trends, such as the growth of e-commerce and a growing need for tower infrastructure, and our strategy is to participate in the aforementioned secular trends while continuing to be mindful of the two primary factors that negatively impact real estate returns: new supply and leverage. We believe these trends are underappreciated and seek to exploit this inefficiency, while actively searching for pockets of value. Our holdings are diversified by property type and are a mix of offense and defense. Examples of offensive holdings include data centers, towers, and industrial property types, while defensive property types include medical offices, triple-net lease real estate, apartments, and student housing.

The yield available in these areas is generally offsetting some of the risk associated with owning these investments. The risk may manifest in volatility and depressed prices that can be exacerbated by a lack of liquidity. Understanding this and focusing on securities that can and will continue to pay their stated income is an important consideration and one where rigor, careful underwriting of each investment and unique insight, and risk management can all come together to produce sustainable income and attractive returns for investors.

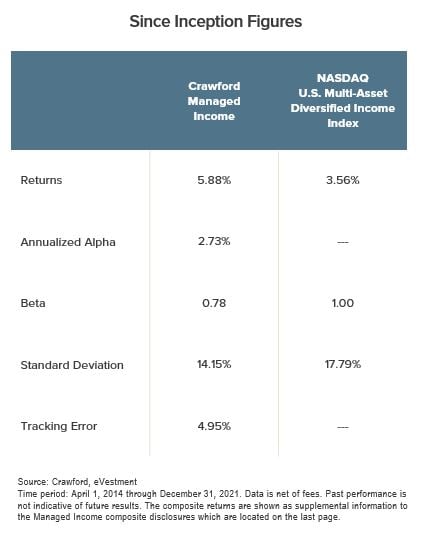

It should be reiterated that many of the opportunities outlined above are a function of individual investors trafficking in most of these securities. Often, we find ourselves in a position where we possess an analytic and risk management advantage. We seek to use our information advantage while taking advantage of the illiquidity and higher yield that comes along with investing in these asset classes. As far as our results go, we believe they speak for themselves. Since inception, we have generated positive alpha with a lower standard deviation relative to our benchmark, the Nasdaq U.S. Multi-Asset Diversified Income Index Fund, which holds the aforementioned five asset classes.

Disclosures:

Crawford Investment Counsel is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Crawford Investment Counsel, including our investment strategies, fees and objectives, can be found in our Form ADV Part 2, which is available upon request.

The widely recognized benchmark(s) in this presentation are used for comparative purposes only. The NASDAQ U.S. Multi-Asset Diversified Income Index is designed to provide exposure to multiple asset segments, each selected to result in a consistent and high yield for the index. The Index is comprised of securities classified as U.S. equities, U.S. Real-Estate Investment Trusts (REITs), U.S. preferred securities, U.S. master-limited partnerships (MLPs) and a high yield corporate debt Exchange-Traded Fund (ETF). The volatility (beta) of the portfolios may be greater or less than the benchmarks. It is not possible to invest directly in these indices.

CRA-22-065

An Attractive In-Plan Income Solution

For 401(k) participants seeking income, we believe the Crawford Managed Income Strategy is an attractive solution.

Shining Light on Retirement Income

One of the significant, real-world issues with investing in retirement is consistency and reliability of income.

High and Rising Income: Crawford Dividend Yield Strategy

In this strategy, growth of income is achieved by owning companies that increase dividends regularly, and it is buttressed by our active management process.