Let’s start by breaking down what the acronym “T-CRUT” means. The T stands for Testamentary, which means the CRUT is set up upon the death of the grantor. CRUT stands for Charitable Remainder Unitrust, which is the type of trust that is set up. A CRUT takes an asset such as stocks, real estate, or a retirement account in this case, and provides an income stream to the income beneficiary(ies) for a period. Once the term or the life of the beneficiary(ies) has passed, the remaining assets go to a charity originally designated by the donor. The present value (value in today’s dollars) of this remaining amount given to charity must be at least 10% of the initial value of the trust.

For some investors with sizable IRA balances, T-CRUTs can be a useful strategy that blend tax efficiency, income, control, and philanthropic intent. In this piece, we explore how a T-CRUT compares to the typical 10-year inherited IRA distribution, and how T-CRUTs can serve as a targeted solution to address the compressed distribution timeline now required under the SECURE Act while preserving income benefits and supporting charitable goals.

Prior to the SECURE Act, an IRA inherited by non-spouse beneficiaries was allowed to ‘stretch’ distributions over their life expectancy. This allowed the inheritor to have a long period of tax deferral and required annual distributions that were easy to digest from a tax perspective. However, the SECURE Act reduced the period for most inheritors of the next generation to liquidate the IRA balance to just ten years. While there is nuance to this, our explanations in this piece assume a generic scenario whereby the IRA is left from one generation to the adult child(ren) of the next, with a 10-year period to distribute.

As you might imagine, the 10-year payout requirement can create burdens for several reasons. For one, adult children are likely in their peak earnings years by the time they inherit the IRA. Therefore, the compressed distribution timeline can potentially push them into higher marginal tax brackets. Lastly, the thought of leaving a large IRA outright to heirs may be problematic for some. For those with charitable intent, those with a desire to artificially ‘stretch’ the distribution period, or those who are concerned about leaving significant IRA assets to their heirs untethered, a T-CRUT can be a compelling option.

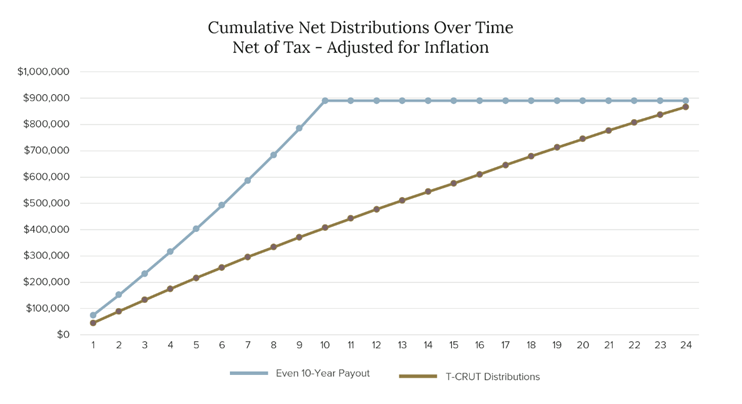

As an example of how this could potentially look, let’s assume an IRA is left to a T-CRUT and compare that to the typical 10-year payout. To make things simple, let’s assume the distribution rate and the growth rate of the T-CRUT are both 6.5% annually. Our scenario will also assume a $1,000,000 IRA, a 2.5% annual inflation rate, a 30% income tax rate, and a 20% capital gains tax rate. This should be of no surprise, but the net-of-tax cumulative distributions for the 10-year inherited IRA outpaced the T-CRUT, adjusted for inflation. In other words, with a T-CRUT, it would take roughly 24 years to distribute what could be distributed evenly over 10 years.

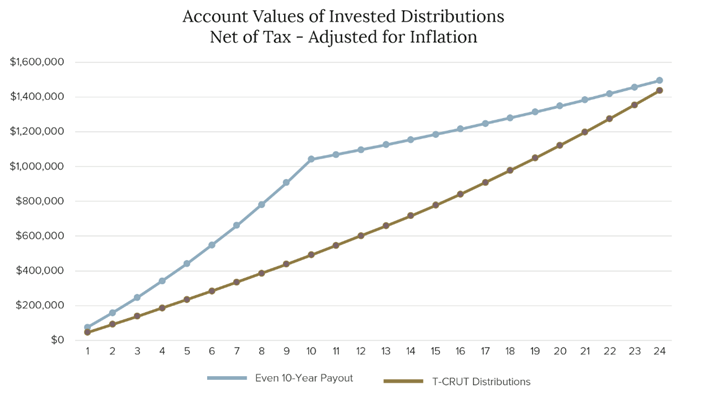

If we instead focus our attention on cumulative wealth transfer to the next generation, rather than income, we see similar outcomes. We can make this analysis by assuming the after-tax proceeds in both cases would be reinvested into a non-retirement investment account over the same period:

While a T-CRUT offers a way to extend the payout period beyond the SECURE Act’s 10-year distribution requirement, it is not without tradeoffs. One key consideration is the timing of cash flows. Under the standard 10-year rule, beneficiaries receive larger distributions up front, which, if reinvested in a taxable brokerage account, begin compounding immediately. By contrast, a T-CRUT typically pays out a smaller income stream over a much longer period. The effect is that beneficiaries have less capital available to invest early on, and thus miss out on the “time in the market” advantage that larger, earlier distributions would have provided. In other words, the T-CRUT essentially trades higher near-term distributions and their compounding benefit for a smoother, longer income stream tied to life expectancy or a set term.

Another consideration is that if transferred outright, the beneficiary has the option, not the requirement, to spread distributions over a 10-year period, but could theoretically distribute it all immediately. Any wealth left over upon the death of the inheritor would go to whomever they choose. Moreover, upon the death of the income beneficiary (or end of the CRUT term), the remaining assets in the T-CRUT would pass to charity. Therefore, the age and health of the income beneficiary should be considered. Fortunately, naming a T-CRUT as a beneficiary of an IRA can easily be changed if/when circumstances change. It is also important to note that the grantor of the T-CRUT would receive an estate tax deduction upon their death, equal to the present value of the remainder interest (amount that is expected to go to charity). Taxation of income from CRUTs is ‘worst-in, first-out,’ meaning ordinary income is distributed first, then more favorable capital gains and dividends, then tax-free income, and finally return of principal. In other words, taxes are not eliminated, they are deferred.

In conclusion, the T-CRUT should be seen as a niche strategy, rather than a perfect tool to save taxes and transfer wealth. As with all estate strategies, the appropriateness of a T-CRUT depends on your individual circumstances and legacy wishes. Individuals who consider T-CRUTs are often those who:

Crawford’s long history of investing thoughtfully with a focus on growth and income is aligned with the long-term objectives of charitable remainder trusts. By focusing on both capital appreciation and consistent income generation, we aim to support the dual goals inherent in these trusts: providing reliable distributions to beneficiaries and preserving (or enhancing) the remainder value for charitable giving. Our quality-focused approach seeks to provide both capital appreciation and a natural stream of income, which can help sustain required distributions without eroding principal. If you would like to consider a T-CRUT as part of your broader estate plan, we encourage you to reach out to our team to explore how we can help you achieve your goals. As always, these decisions should be made in collaboration with your tax and estate planning professionals to ensure the best outcome for your unique situation.

Footnote & Disclosure: